Table of Contents >> Show >> Hide

- What Fundrise Means by an “Internet Public Offering”

- How the Fundrise iPO Works (Plain-English Edition)

- The Bull Case: Why Some Investors Like the Fundrise iPO

- The Bear Case: Risks You Should Take Seriously

- A Practical Due-Diligence Checklist Before You Click “Invest”

- Who Might Consider the Fundrise iPO (and Who Probably Shouldn’t)

- Three Example Decision Frameworks (Use the One That Sounds Like You)

- If You’re Under 18 (Quick Reality Check)

- Conclusion: Treat the Fundrise iPO Like a Long-Term, Illiquid Venture Bet

- Bonus: Real-World Experiences (What Investors Commonly Learn the Hard Way)

Fundrise has a knack for taking intimidating Wall Street phrases and turning them into something you can click on between emails.

“Internet Public Offering” (or “iPO”) is one of those phrases. It sounds like a classic IPOcue the bell ringing, confetti, and a ticker symbol.

But Fundrise’s iPO is its own animal: a way for everyday investors to buy shares in the parent company behind Fundrise, directly through Fundrise’s platform.

So… should you invest?

The honest answer is: it depends on why you’re buying it, how much you’re buying, and whether you’re comfortable treating it like a long-term,

illiquid “venture-style” bet rather than a normal stock you can flip next Tuesday.

This guide breaks down how the Fundrise iPO works, what drives potential returns, the biggest risks (including the ones people gloss over),

and a practical framework you can use to decide whether it belongs in your portfolio.

(Spoiler: “because it feels cool to own a piece of the platform” is a real reason… just not a complete one.)

What Fundrise Means by an “Internet Public Offering”

It’s “public,” but not the way most people mean “IPO”

In a traditional IPO, a company “goes public” by listing shares on a stock exchange, typically with underwriters (big banks) setting an offering price,

allocating shares, and then letting the stock trade freely in the public market.

Fundrise’s iPO is different. It’s a Regulation A offeringan exemption that allows companies to raise money from the public

without doing a full, traditional SEC-registered IPO. Regulation A has tiers, and Tier 2 (commonly used for broader retail participation)

permits offerings up to a defined annual limit and comes with required disclosures and ongoing reporting. In other words:

it’s regulated and real, but it’s not “listed on the NYSE tomorrow.” The experience is more like buying into a private company offering

that happens to be open to the public.

What you’re actually buying

The Fundrise iPO lets investors purchase shares in Rise Companies Corp., the parent company of Fundrise.

That means your investment results depend on how the Fundrise business performs as a companynot on the returns of any specific Fundrise real estate fund.

Think of it like owning shares in the “store,” not just buying the “products” on the shelves.

That distinction matters because Fundrise’s real estate funds can do fine in a given year while the parent company’s growth slows (or vice versa).

You’re investing in the platform’s long-term business value: revenue, costs, product expansion, customer growth, and the odds of a future liquidity event.

How the Fundrise iPO Works (Plain-English Edition)

1) It’s a Regulation A offering with an offering circular

Instead of a classic IPO prospectus and exchange listing, Reg A offerings use an offering circular.

That document is where the “real” details live: risk factors, use of proceeds, financial statements, and how the securities work.

If you’re deciding whether to invest, reading (or at least scanning) the offering circular isn’t optionalthis is where the fine print graduates

from “fine” to “life choices.”

2) Share price is set by the board, not discovered by a market

In a traditional IPO, underwriters help set the initial price, and then the market takes over once shares trade.

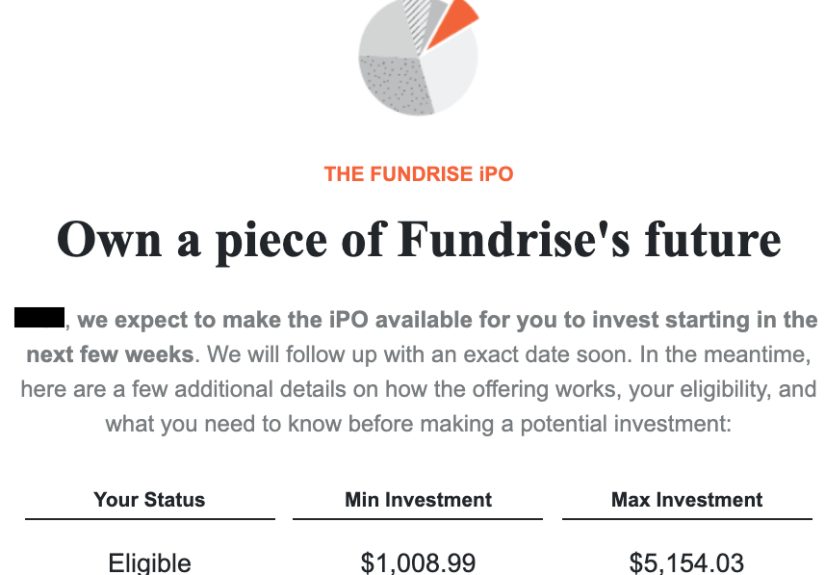

In the Fundrise iPO, the per-share price is determined by the company’s board and can be adjusted over time.

Fundrise has publicly discussed updating the iPO share price periodically (for example, sharing a specific per-share price in an investor update).

Translation: you don’t get real-time “price discovery” from a public market.

The number you see is best understood as an internal valuation signal based on the company’s view of its progress and prospects,

rather than a quote produced by thousands of buyers and sellers.

3) Liquidity is limited (and that’s not a small footnote)

This is the part many investors emotionally acknowledge and then immediately forget.

Fundrise iPO investors should expect to hold the investment for a long time, and potentially indefinitely,

until a liquidity event occurs (like a sale of the company or a traditional IPO)and none of that is guaranteed.

There are also restrictions on transferability and mechanisms that can limit your ability to sell.

Even when a company offers a redemption/repurchase feature, those programs can be limited, suspended, or unavailable at times.

If you invest, assume this money is “locked up” in practice.

4) Returns may come from a future liquidity event, not dividends

Fundrise has indicated that the iPO investment is not designed like an income vehicle and does not necessarily expect to pay dividends.

That means your “win” scenario is typically:

- Valuation increases over time (reflected in updated share price), and/or

- A liquidity event where shares can be sold (sale of the company, traditional IPO, or another exit pathway).

Your “meh” scenario is years of waiting while the business grows slowly.

Your “ouch” scenario is that the company underperforms, valuations drop, or you simply never get a clean exit window when you want it.

The Bull Case: Why Some Investors Like the Fundrise iPO

You believe in the business, not just the investments

Fundrise didn’t just build a product; it built a distribution engine: a direct-to-investor platform with recurring relationships.

If you believe the platform will keep expanding (real estate, private credit, venture-style products, and new structures),

then owning a slice of the parent company can feel like owning the “operating system” behind a growing set of investment products.

You want long-term optionality

Many private-company investors accept a simple trade:

less liquidity now in exchange for more potential upside later.

The iPO can be seen through that lens: you’re buying optionality on a future liquidity event at a valuation you consider reasonable today.

You like alignment (and a bit of nerdy pride)

Some investors value alignmentbeing both a customer and an owner.

It’s the same energy as buying stock in a company whose products you use daily,

except with more paperwork and fewer memes.

The Bear Case: Risks You Should Take Seriously

Illiquidity risk is real, and it changes everything

Illiquidity isn’t just “I can’t sell today.”

It’s also:

- Not being able to rebalance when your portfolio drifts.

- Not being able to harvest losses when you want to.

- Not being able to respond to life events (job change, emergency, big purchase).

- Having to accept a redemption window that may be limited, paused, or priced differently than you hoped.

In short: illiquidity turns a financial decision into a lifestyle decision.

Valuation uncertainty (a.k.a. “the number is not a stock quote”)

With publicly traded stocks, you get constant price discovery. Here, the per-share price is set internally and updated periodically.

That doesn’t automatically make it “bad,” but it does mean you should be cautious about treating displayed gains as the same kind of gains

you’d have in a liquid public stock.

Business-model risk and macro risk

Fundrise operates in markets that are sensitive to interest rates, credit conditions, and investor sentimentespecially around real estate and private assets.

Even if the underlying funds are diversified, the platform’s growth can slow in tough markets:

fewer new investors, lower inflows, higher customer acquisition costs, and pressure on fee revenue.

If you’re investing in the parent company, you’re exposed to the health of the business across cycles.

A great company can still have a rough decade if the macro environment refuses to behave.

Dilution and governance

Many private-company-style investments involve dilution over time as the company raises more capital.

You should understand:

- What class of shares you’re buying and what rights it has.

- How future fundraising could affect your ownership percentage.

- Who controls major decisions (voting rights can vary by class).

This isn’t unique to Fundriseit’s standard startup mathbut you need to be okay with it before you invest.

Regulatory and operational complexity

Reg A offerings require disclosures and ongoing reporting, but they are not the same as a fully exchange-traded public company.

That means information can be less “headline friendly,” and analyzing it can feel like doing your taxes with a flashlight.

If you don’t plan to read filings or updates, you’re choosing to invest with less visibilityown that choice.

A Practical Due-Diligence Checklist Before You Click “Invest”

Step 1: Read the offering circular like a strategist, not a lawyer

You don’t need to memorize it. You do need to know where the landmines are.

Focus on:

- Risk factors: especially liquidity, valuation methodology, and business concentration risks.

- How the share price is determined: what it is (and what it isn’t).

- Transfer and redemption limitations: when, how, and under what conditions liquidity may be available.

- Use of proceeds: what your investment money actually funds.

- Financials: revenue trends, expenses, cash burn (if any), and runway.

Step 2: Know what “success” looks like for this investment

Ask yourself: What needs to happen for me to feel good about this five years from now?

Examples:

- The company reaches sustained profitability (or a clear path to it).

- Assets on the platform grow significantly and stick (not just one-time spikes).

- Product expansion succeeds without blowing up costs.

- A credible liquidity path emerges (even if it’s years away).

Step 3: Run the “can I live without this money?” test

This is the most important question, and it’s boring on purpose:

If this money were locked up for 7–10+ years, would I still be okay?

If not, the investment size is too largeor the investment is the wrong fit.

Step 4: Decide your position size using a simple rule

Many experienced investors treat illiquid private-company bets as a small slice of their overall portfolio.

A common approach is to size it as “money I can afford to be wrong about” while still taking it seriously.

If you’re tempted to make it a huge portion because you’re excited, that’s usually a sign you should shrink it.

Who Might Consider the Fundrise iPO (and Who Probably Shouldn’t)

This might be a fit if:

- You already use Fundrise and believe in the long-term growth of the platform.

- You can commit to a long holding period without needing liquidity.

- You understand that valuation updates aren’t the same as a liquid market price.

- You’re comfortable with private-company-style risk, including the possibility of partial or total loss.

This is probably not a fit if:

- You need flexibility, emergency access, or near-term cash options.

- You’re investing mainly because it “feels like an IPO pop.”

- You aren’t willing to read offering materials or company updates.

- You’ll lose sleep if the value doesn’t move (or moves down) for long stretches.

Three Example Decision Frameworks (Use the One That Sounds Like You)

1) The “Power User”

You invest with Fundrise regularly, you understand the product lineup, and you like the company’s approach.

For you, the iPO is a “support + upside optionality” investment. Your best move is to keep it small, treat it as long-term,

and focus your decision on business fundamentals rather than vibes.

2) The “Skeptical Analyst”

You’re open to the idea, but you want evidence. Your version of due diligence should be heavy on filings and metrics:

revenue trajectory, costs, and whether the company is building durable advantages.

If you can’t get comfortable with valuation mechanics and liquidity constraints, skip it without guilt.

3) The “Diversifier”

You already have broad public-market exposure and you’re exploring alternative investments for long-term growth.

Your decision should be portfolio-driven:

pick a small allocation, assume illiquidity, and monitor it like a private holding (annually, not daily).

If You’re Under 18 (Quick Reality Check)

Many investment accounts in the U.S. require you to be an adult to open directly.

If you’re under 18 and interested in investing, this is typically done through a parent/guardian using a custodial structure.

The right move is to talk it through with a parent/guardian and make sure any investment fits your family’s plan and risk tolerance.

Conclusion: Treat the Fundrise iPO Like a Long-Term, Illiquid Venture Bet

The Fundrise iPO can make sense if you’re investing for the right reasons: long-term belief in the business, comfort with illiquidity,

and a willingness to hold through uncertainty.

It’s not a substitute for diversified public-market investing, and it’s not a “quick flip” IPO story.

It’s closer to owning a piece of a private company with regulated disclosuresand all the patience that implies.

If you decide to invest, the best “foolproof” strategy is actually pretty unsexy:

size it small, read the documents, assume you can’t sell when you want, and give it time.

If that sounds like a dealbreaker, congratulationsyou just saved yourself from the most common mistake in private investing.

Bonus: Real-World Experiences (What Investors Commonly Learn the Hard Way)

Let’s talk about the part people usually discover only after they’ve invested: the experience of owning an illiquid “almost-public” share.

Not the theory. The lived realityminus the melodrama and plus a little practicality.

First, many investors report that the emotional rollercoaster is… oddly quiet. With public stocks, your account value updates constantly,

giving you a steady drip of dopamine (or panic). With an iPO, you might see the share price updated only occasionally.

That can feel peaceful at firstlike investing without the noise.

Then it can feel confusing: “Wait, how is the company doing right now?” The lesson: your job shifts from watching a ticker

to reading updates and filings, because that’s where the story lives.

Second, people often underestimate how much liquidity affects confidence. Investors commonly start out thinking,

“I’m a long-term investor, I don’t need liquidity.” And that might be trueuntil life happens.

A surprise expense, a job change, a move, a tuition bill, a new baby, a medical deductible with an attitude.

Suddenly, “long-term” becomes “I would like my money to do a quick U-turn, please.”

Illiquid investments aren’t bad; they’re just honest. They reveal whether your emergency fund and planning were actually ready for adulthood.

Third, some investors learn that “estimated value” and “cash I can receive” are not the same thing in private-style holdings.

When you see a higher per-share price, it can feel like winning. But if there’s no active market,

you haven’t truly tested what someone else would pay you for those shares today.

That doesn’t mean the value is fake; it means it’s unproven until a real liquidity event or a functioning secondary market exists.

The most level-headed investors treat the displayed value as informational and keep their expectations anchored to fundamentals,

not just the on-screen number.

Fourth, investors often discover that the biggest “return” early on is psychological: the feeling of being aligned with a company they use.

There’s a genuine satisfaction in being both a customer and an owner, especially when you believe the company is building something useful.

The healthier version of that mindset is: “I like this company, so I’ll make a small, sensible bet.”

The unhealthy version is: “I like this company, so I’m going to make it my entire personality and 40% of my net worth.”

Be the first person. The first person sleeps better.

Finally, long-term holders often say the investment becomes easiest when they stop trying to treat it like a public stock.

The best experience is usually: invest an amount you can truly set aside, check in periodically,

and evaluate progress based on business execution and disclosed metricsnot day-to-day vibes.

If a liquidity event happens, great. If it takes longer, you didn’t build your financial plan around a maybe.

That’s what “smart optionality” looks like in real life.