Table of Contents >> Show >> Hide

- What “Boring” Actually Means in Bond Investing

- Bond Math: The Tug-of-War Between Prices, Yields, and Interest Rates

- The Risks People Forget: Inflation, Credit, and the Temptation to Tinker

- Bonds’ Real Job: Diversification and Staying Power

- Picking Your Flavor: Treasuries, Munis, Corporates, TIPS, I Bonds, and Bond Funds

- Bond Funds vs. Individual Bonds: Two Different Versions of “Boring”

- Practical Ways to Keep Bonds Boring (In the Best Way)

- Conclusion: Embrace the Snooze Button

- Extra: of Real-World Experiences with “Boring” Bonds

Bonds don’t get the Hollywood treatment. They don’t explode. They don’t teleport. They rarely get a standing ovation.

And that’s the point.

The best “fixed income” is basically the financial equivalent of a good refrigerator: it hums in the background, keeps the important stuff safe,

and only becomes “interesting” when it stops doing its job. Ben Carlson’s famous ideabonds are supposed to be boringisn’t a dunk on bonds.

It’s a compliment. In a world where every headline tries to turn your portfolio into a reality TV show, boring is a feature.

What “Boring” Actually Means in Bond Investing

A bond is an IOU. You lend money to a government, municipality, or company, and in exchange you (usually) get regular coupon payments and your principal back at maturity.

That’s it. No plot twists required. The goal isn’t to “go viral.” The goal is to be a stabilizeran anchor that can help you stay invested when stocks are acting like

they drank three energy drinks and decided to start a band.

In practical terms, “boring” usually means:

- More predictable cash flow than stocks (coupon payments are scheduled, not hoped for).

- Typically lower volatility than equities, especially in high-quality bonds.

- A role in risk management: diversification, capital preservation, and funding near-term goals.

If your bond allocation is constantly thrilling you, it might be doing something other than “bond stuff.” (And yes, we’re politely side-eyeing

anything with the words “high yield” and “can’t miss” in the same sentence.)

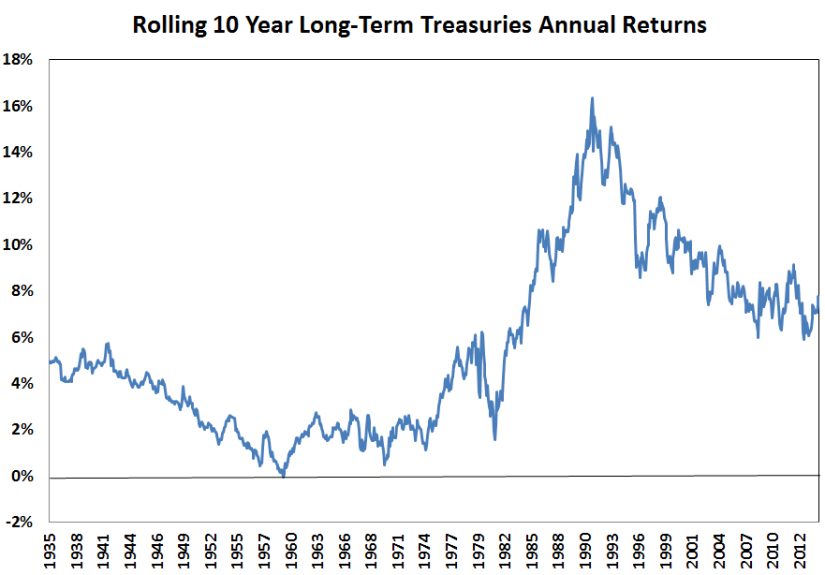

Bond Math: The Tug-of-War Between Prices, Yields, and Interest Rates

Bonds feel confusing until you learn their one main magic trick: bond prices and interest rates move in opposite directions.

When prevailing rates rise, older bonds with lower coupons become less attractive, so their prices fall. When rates fall, older bonds with higher coupons look better,

so their prices rise. It’s not dramait’s math.

A simple example (with numbers that won’t ruin your day)

Imagine you own a bond that pays a 2% coupon. Then new bonds start paying around 5%. If you tried to sell your 2% bond today, a buyer would likely say,

“Sure… but only if the price drops enough so my total return lines up with the new market yield.” That price adjustment is how the market restores balance.

This is why people can see bond fund values dip when rates riseeven if the bonds inside the fund keep paying interest. The market is repricing the existing bonds

so new buyers get competitive yields, while current holders experience price volatility along the way.

Duration: the “sensitivity knob” for interest rate risk

If you want one word that explains why some bonds feel chill and others feel like they’re practicing for a trampoline competition, it’s duration.

Duration estimates how sensitive a bond (or bond fund) is to changes in interest rates.

- Longer duration generally means more price movement when rates change.

- Shorter duration generally means less price movement when rates change.

A rough rule of thumb often used in education is: if a portfolio has a duration of about 5 years, a 1% rise in rates might translate into roughly a 5% price decline,

all else equal. It’s an approximation, but it’s useful for understanding the “feel” of a bond portfolio.

“Boring bonds,” for many investors, means keeping duration aligned with the time horizon and the job the money needs to do.

The Risks People Forget: Inflation, Credit, and the Temptation to Tinker

Inflation risk: the quiet bond villain

A big reason bonds look safe is that they can be structured to return principal at maturity. But what matters in real life isn’t just getting your dollars back

it’s what those dollars can buy. Inflation can quietly take a bite out of “safe” returns, especially over long periods.

Carlson’s point (based on long-term data) is that nominal bond returns can look steady over long stretches, but real returns (after inflation)

can be far less comforting. Translation: bonds can be “safe” and still disappoint you in purchasing-power terms.

Credit risk: boring until it isn’t

Treasuries are generally considered lower credit risk because they’re backed by the U.S. government’s ability to pay. Corporate bonds can offer higher yields,

but they introduce the possibility that the issuer struggles or defaults. Municipal bonds add tax considerations and local credit factors.

The classic trade-off is simple: higher yield usually comes with higher risk, and not just the “my line went down today” kind of risk.

The temptation trap: market timing in a tuxedo

Bonds can also tempt people into constant guessing: “Rates will rise, so I should wait,” or “Rates will fall, so I should load up on long-term bonds.”

The problem is that predicting interest rates consistently is hard, and chasing forecasts can turn a stabilizer into a stress generator.

If bonds are the boring part of the portfolio, treating them like a casino game defeats the purpose. (If you want adrenaline, try assembling furniture without

reading the instructions. Same thrill, cheaper.)

Bonds’ Real Job: Diversification and Staying Power

Bonds and bond funds are often used to diversify a portfolio because they tend to behave differently than stocks. Not always. Not perfectly.

But often enough that they can reduce overall portfolio volatility and help investors stay disciplined.

Think of bonds as the portfolio’s shock absorbers. They don’t stop every bump, but they can keep you from launching through the windshield when markets get rough.

Why “boring” matters during stressful markets

In down equity markets, many investors discover the true value of a steady fixed income allocation: it can provide liquidity for spending needs,

rebalancing opportunities, andmost underrated of allemotional stability.

A portfolio plan is only as good as your ability to follow it. Bonds can help keep the plan followable.

But bonds aren’t magic (see also: 2022)

Plenty of investors were surprised when bonds had a rough stretch as rates rose quickly. That period was a loud reminder that bonds carry interest rate risk,

and longer-duration bonds can be volatile when yields reset higher.

The lesson wasn’t “bonds are broken.” The lesson was “bond math still works.” When yields rise, prices adjust. Over time, higher yields can improve the income

component of total returnespecially for investors who are reinvesting coupons and staying the course.

Picking Your Flavor: Treasuries, Munis, Corporates, TIPS, I Bonds, and Bond Funds

“Bonds” is a category, not a single product. Choosing fixed income is like ordering coffee: you can get something mild and predictable, or you can ask for a

triple-shot espresso with a motivational speech. Both are coffee. Only one is a calm morning.

U.S. Treasuries: bills, notes, and bonds

Treasury bills are short-term (typically a year or less), Treasury notes run out to around 10 years, and Treasury bonds extend longer (commonly 20–30 years).

Notes pay interest every six months and mature in set terms like 2, 3, 5, 7, or 10 years. These are often considered the “plain bagel” of the bond world:

not flashy, widely used, and surprisingly important.

Municipal bonds: the tax-angle cousin

Munis can offer tax advantages depending on where you live and your tax situation. They can be helpful, but they’re not automatically risk-free.

Credit quality varies by issuer, and prices still respond to rate changes.

Corporate bonds: more yield, more credit homework

Investment-grade corporates tend to be “boring-er” than high-yield bonds, which can behave more like stocks during economic stress.

If you’re using bonds as ballast, it helps to remember that not all bonds actually float the same way.

Inflation-linked bonds: TIPS and I Bonds

Inflation-linked bonds exist for one main reason: inflation is a real risk. TIPS adjust principal with inflation measures, while Series I savings bonds

use a composite rate that includes an inflation component and have purchase limits and holding rules. They can be useful tools, especially for investors

who want inflation protection in the “safe money” bucketso long as you understand the constraints.

Bond funds and bond ETFs: diversification in a box

Bond funds can offer instant diversification across many issuers and maturities. The trade-off is that most bond funds don’t “mature” the way an individual bond does.

Their net asset values can fluctuate, and the fund is constantly replacing maturing bonds with new ones.

That’s not bad. It’s just different. The key is matching the tool to the goal.

Bond Funds vs. Individual Bonds: Two Different Versions of “Boring”

Investors often say, “I’ll just hold my bonds to maturity so I don’t lose money.” That logic applies cleanly to individual bonds you actually hold to maturity

(assuming the issuer pays). But bond funds don’t work the same way because they typically don’t have a set maturity date. Their value changes daily, and

“holding to maturity” isn’t an option in the literal sense.

So how do you think about a bond fund? Instead of focusing on maturity, focus on:

- Duration (how sensitive the fund is to rate changes)

- Credit quality (how much default risk is in the mix)

- Costs (fees matter more when expected returns are modest)

- Role in the portfolio (income, stability, diversification, or a specific liability)

In other words, if you want bonds to be boring, you don’t pick them by vibes. You pick them by job description.

Practical Ways to Keep Bonds Boring (In the Best Way)

Here are time-tested, common-sense approaches that help keep fixed income from turning into “fixed income… and fixed anxiety.”

1) Match duration to your time horizon

If the money is needed soon, short-duration bonds (or similar low-volatility fixed income) can reduce interest rate risk.

If the goal is long-term diversification, intermediate-duration high-quality funds are often used as a middle ground.

2) Consider a bond ladder for predictable cash flows

A bond ladder staggers maturities over time. When a rung matures, you can reinvest at current rateshelping manage reinvestment risk and reducing the urge to time rates.

Ladders can be especially appealing for investors funding near-term spending needs because they create a schedule of maturing principal.

3) Don’t confuse “higher yield” with “free lunch”

If you’re using bonds to stabilize a portfolio, loading up on lower-quality credit may defeat the purpose. Higher yields are real, but so are defaults,

downgrades, and equity-like drawdowns during stress.

4) Diversify across issuers and sectors

Diversification doesn’t eliminate risk, but it can reduce the damage of any single issuer, sector, or surprise headline. Broad bond index funds (or diversified

bond fund strategies) are popular for a reason: they make “boring” easier to maintain.

5) Rebalance like an adult

Boring bonds shine when you use them to rebalance. When stocks run hot, you trim equities and add to fixed income. When stocks fall, your bond allocation

can be a source of funds to buy equities at lower priceswithout panic-selling.

The overall theme is simple: bonds aren’t there to win the talent show. They’re there to keep the entire portfolio from falling apart when the bass drops.

Conclusion: Embrace the Snooze Button

If you want a portfolio you can stick with, you need at least one part of it that doesn’t demand constant attention. Bondsespecially high-quality fixed income

can provide income, diversification, and stability, even though they come with interest rate risk and inflation risk.

The wealth-of-common-sense takeaway is this: when bonds are doing their job, they often feel boring. That’s not a flaw.

That’s the sound of your plan working.

So yes, bonds are supposed to be boring. Let them be boring. Save your excitement for things that deserve itlike finding an extra fry at the bottom of the bag.

Extra: of Real-World Experiences with “Boring” Bonds

Most investors don’t fall in love with bonds at first sight. It’s usually a slower romancemore “reliable neighbor who waters your plants” than “mysterious stranger

in a leather jacket.” The bond appreciation phase often begins the moment someone tries to live through a truly chaotic stock market while also needing cash for

real-life expenses: rent, tuition, a car repair, a down payment, or retirement withdrawals that don’t care what the S&P 500 did this morning.

One common experience: investors build a portfolio that’s 100% stocks because they’re young, confident, and fueled by optimism (and sometimes by TikTok).

Then a rough market arrives and suddenly the “all-equity” plan becomes a psychological endurance test. That’s when bondsespecially short- or intermediate-duration

high-quality holdingsstart to feel less like “dead money” and more like “sleep at night money.”

Another classic experience shows up when rates rise. People see bond fund values drop and assume the worstuntil they realize what’s happening under the hood.

The fund’s older, lower-coupon bonds get repriced downward, but new bonds entering the portfolio often come with higher yields. Over time, higher income can help

rebuild total return. The lesson feels counterintuitive at first: a bond fund can lose money today while becoming more attractive for future expected income.

That’s not a loophole. That’s the bond market doing bond-market things.

Investors who use bond ladders often describe a different kind of calm. They’re not trying to guess rates; they’re building a schedule. A rung matures,

cash arrives, decisions get made. If rates are higher, reinvestment is easier. If rates are lower, at least some longer rungs were locked in earlier.

This kind of structure is especially comforting for goal-based moneylike saving for a home purchase in two years, or covering the first few years of retirement

spending.

Inflation-linked products create another set of “bond experiences.” Some people discover I Bonds during inflation spikes and love the idea of inflation-adjusted

returns and tax advantages, then later learn about purchase limits and the rules around holding periods. The experience becomes a reminder that even the “safe”

corner of investing has detailsfine print, not fireworks.

The most useful bond experience, though, is the one that doesn’t make headlines: rebalancing. Investors who stick with a plan often recall moments when bonds

gave them the courage (and the liquidity) to buy stocks after a drop. In that sense, boring bonds sometimes do the most exciting thing of all:

they help you act rationally when everyone else is auditioning for a panic montage.

Over time, many investors stop asking, “How do I make bonds exciting?” and start asking, “How do I keep my bond allocation doing its quiet job?” That’s when

the portfolio starts to feel less like a guessing game and more like a systemone that can survive real life, not just a backtest.