Table of Contents >> Show >> Hide

- What “Declined” Actually Means (It’s Not Always About Money)

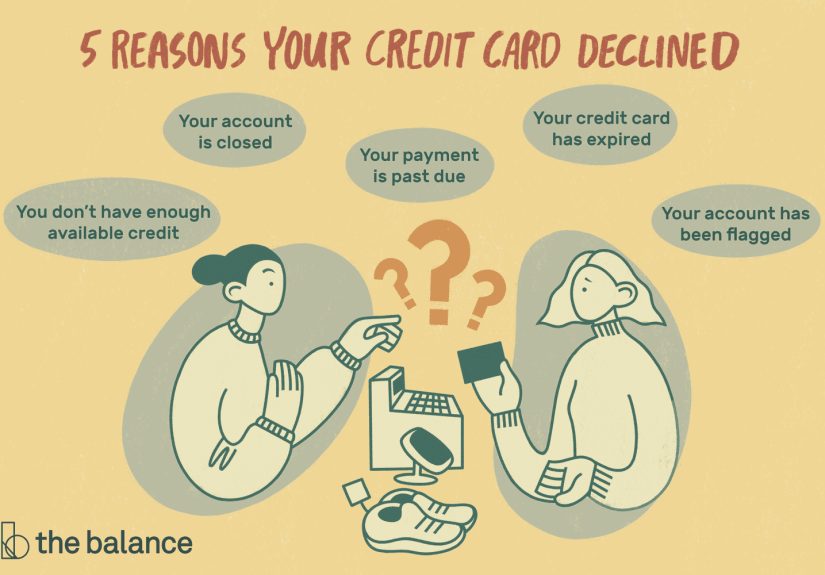

- The Most Common Reasons Your Credit Card Was Declined

- 1) You Hit Your Credit Limit (Or a Transaction Would Push You Over)

- 2) The Merchant Ran a Preauthorization Hold (Gas Stations and Hotels Love These)

- 3) Your Bank Flagged the Purchase as Potential Fraud

- 4) You Entered Incorrect Information (Online Purchases Are Extra Sensitive)

- 5) Your Card Is Expired (Or You Forgot to Activate the Replacement)

- 6) Your Card Was Locked, Frozen, or Restricted

- 7) The Transaction Type Isn’t Allowed (International, Cash-Like, or Subscription Issues)

- 8) The Merchant’s System Glitched (It’s Not Always Your Card’s Fault)

- 9) Your Issuer Sent a Generic “Do Not Honor” Style Decline

- 10) You’re Using an Old Stored Card for a Subscription (And the Details Changed)

- What to Do When Your Card Gets Declined (Without the Panic Spiral)

- Declined in Specific Situations: Quick Fixes That Often Work

- How to Prevent Future Declines (A Little Prep Goes a Long Way)

- Bottom Line

- Common Experiences: “Yep, That Happened to Me” (Real-World Scenarios)

Few modern moments are as humbling as a credit card decline. One second you’re confidently tapping to pay; the next, the checkout screen politely informs you that you and your payment method are “taking some time apart.”

The good news: a decline usually isn’t a personal attack. It’s a quick “no” from a system designed to prevent fraud, limit risk, and catch honest mistakeslike typing your ZIP code with the enthusiasm of a raccoon on a keyboard.

This guide breaks down the most common reasons credit cards get declined, what’s happening behind the scenes, and what to do nextwithout panicking, apologizing to the cashier, or moving to a new city under a different name.

(You can stay. It happens to everyone.)

What “Declined” Actually Means (It’s Not Always About Money)

A card transaction has a few players: the merchant (store or website), the payment processor and card network (the “pipes”), and your card issuer (the bank that issued your card).

A decline can come from different points in that chain, but most consumer-facing declines boil down to this: the issuer or the network decided not to approve that specific charge right now.

Sometimes it’s because your account can’t support the purchase (like a maxed-out limit). Sometimes it’s because the system can’t verify you (like a billing address mismatch). And sometimes it’s because technology is technology, and it chose chaos.

Either way, your next steps depend on why the decline happenedwhich isn’t always obvious from the message you see.

The Most Common Reasons Your Credit Card Was Declined

1) You Hit Your Credit Limit (Or a Transaction Would Push You Over)

Even if you have “available credit,” certain transactionstips, deposits, or preauthorizationscan temporarily increase the amount your issuer needs to approve.

If your balance is near the limit, a purchase that seems small can get rejected if it would exceed your available credit once everything is counted.

Example: You try to book a hotel that places a deposit hold plus the room charge. Your card may be declined if the total authorization exceeds your available credit, even if the nightly rate alone looks affordable.

2) The Merchant Ran a Preauthorization Hold (Gas Stations and Hotels Love These)

Some merchants don’t know the final amount at the moment of authorization, so they request a larger “hold” amount first, then finalize the true total later.

This is common at pay-at-the-pump gas stations and with hotels or car rentals. If the hold amount is more than your available credit, the transaction can be declinedeven though you didn’t actually plan to buy $175 worth of gasoline like you’re fueling a space shuttle.

3) Your Bank Flagged the Purchase as Potential Fraud

Fraud prevention systems watch for unusual patterns: a big purchase, a new location, a sudden shopping spree, or a merchant category you rarely use.

If something looks suspicious, your issuer may decline the charge until you confirm it’s you. That’s annoying when you’re buying concert tickets, but it’s helpful when it’s not you buying 14 designer belts at 3:00 a.m.

Example: You usually buy groceries and streaming subscriptions. Then you attempt a high-dollar electronics purchase across the country while traveling. The issuer might decline it and send a “Was this you?” alert.

4) You Entered Incorrect Information (Online Purchases Are Extra Sensitive)

For online or card-not-present purchases, the system often checks details like your billing address, ZIP code, expiration date, or security code (CVV).

A tiny mismatchwrong apartment number, old ZIP code, transposed digitscan trigger a decline.

Example: You moved six months ago but your card issuer still has your old billing address. You enter your new address at checkout, and the issuer declines because it can’t match the details.

5) Your Card Is Expired (Or You Forgot to Activate the Replacement)

Expired cards are a classic. Another common twist: your issuer mailed a replacement card, and your old one stops workingor your new one needs activation.

If you’re still swiping the old card like it’s 2016, the payment system may disagree with your optimism.

6) Your Card Was Locked, Frozen, or Restricted

Many issuers let you lock your card in an app if it’s lost or you want extra protection. If you forgot you turned on that setting, your card can be declined everywhereyes, including your favorite coffee shop that “knows you.”

Also, certain restrictions can apply if your account is past due, under review, or suspected of being compromised.

7) The Transaction Type Isn’t Allowed (International, Cash-Like, or Subscription Issues)

Some cards block specific transaction types (for example, certain international merchants, recurring payments, or “cash-like” transactions) depending on issuer policies and your settings.

The merchant might be fineyour card just isn’t allowed to run that type of charge without additional verification or changes on the issuer side.

8) The Merchant’s System Glitched (It’s Not Always Your Card’s Fault)

Terminals go offline. Payment gateways hiccup. Networks have temporary outages. Chips get dirty. Magnetic stripes get demagnetized.

Sometimes your card is declined because the payment system couldn’t properly process the requestnot because you did anything wrong.

Example: One register declines your card, but another register works. That’s a clue the issue may be the terminal or connection, not your account.

9) Your Issuer Sent a Generic “Do Not Honor” Style Decline

Some declines are frustratingly vaguebasically “no” without a detailed reason. This can happen when the issuer won’t share specifics with the merchant,

or when the decline is tied to risk models, security checks, or internal policies.

In those cases, the only reliable way to learn the reason is to contact your issuer (or check your issuer’s app/alerts) because the merchant often can’t see the details.

10) You’re Using an Old Stored Card for a Subscription (And the Details Changed)

Subscriptions fail all the time because a card expired, got replaced, was locked, or hit a limit at the wrong moment.

Streaming services, app subscriptions, gym membershipsnone of them will hesitate to “pause your access” while you scramble to update billing info.

What to Do When Your Card Gets Declined (Without the Panic Spiral)

Step 1: Try the Simple Fixes First

- Double-check details: Card number, expiration date, CVV, billing ZIP/address (especially online).

- Switch method: Tap if chip fails; chip if tap fails; swipe as a last resort if available.

- Retry once (not five times): A single retry can help if it was a temporary connection issue. Multiple rapid retries can sometimes make fraud systems more suspicious.

- Use a different card or payment method: If you’re in a hurry, this solves the immediate problem while you troubleshoot later.

Step 2: Check Your Issuer App or Messages

Many banks send real-time fraud alerts or “Confirm this purchase” prompts. If you see one, respond quickly.

Approving it can allow you to rerun the transaction successfully.

Step 3: Contact the Card Issuer (Yes, the Number on the Back Works)

If you need the charge to go through (travel, hotel check-in, essential purchase), call your issuer right away.

They can usually tell you whether the decline was due to suspected fraud, a limit issue, a restriction, incorrect verification details, or an account problem.

Step 4: Fix the Root Cause

- If it’s the limit: Pay down the balance (even a partial payment can restore availability once posted), or request a credit line increase if appropriate.

- If it’s a hold issue: Ask the merchant what authorization amount they’re requesting; consider paying inside at the pump, using a different card, or using a smaller prepay amount.

- If it’s fraud prevention: Confirm your identity, update travel settings if offered, and ensure your contact info is current so alerts reach you.

- If it’s wrong billing info: Update your address with the issuer and re-enter the exact billing address on file.

- If it’s a subscription: Update the stored card details and try again after confirming the card is active and unlocked.

Declined in Specific Situations: Quick Fixes That Often Work

Declined Online but Works In-Store

This often points to verification checks (billing address/ZIP mismatch, CVV mismatch), merchant fraud filters, or issuer restrictions on card-not-present transactions.

Try re-entering your billing info exactly as your issuer has it, and confirm the merchant is legitimate (especially if it’s a first-time purchase).

Declined at the Gas Pump

Preauthorization holds can be higher than your final purchase, and that can trigger a decline when available credit is tight.

If it keeps happening, pay inside, use a different card, or choose a smaller prepay amount.

Declined While Traveling

Travel can trigger fraud systems, especially international charges or purchases far from your typical locations.

Check for issuer alerts, confirm the transaction, and keep a backup payment method when possible.

Declined for One Merchant Only

If your card works elsewhere but not at one specific place, the issue might be the merchant’s terminal, network connection, or how the merchant is processing the transaction.

Try another register, another payment type (chip/tap), or ask the merchant to check whether their system is having issues.

How to Prevent Future Declines (A Little Prep Goes a Long Way)

- Keep contact info updated: A working phone number and email help you receive fraud alerts and verification prompts.

- Monitor available credit: Especially before travel, deposits, or large purchases.

- Understand holds: Gas stations, hotels, and rentals may request more than the final amount at authorization.

- Use alerts: Many issuers let you set notifications for large purchases, international transactions, or card-not-present charges.

- Carry a backup: A second card or alternative payment method reduces stress when something unexpected happens.

- Update subscriptions promptly: When you get a replacement card, update any stored payment methods.

Bottom Line

A declined credit card is usually a solvable problem, not a life sentence. Most declines come down to a handful of causes: hitting a limit, verification mismatches,

fraud prevention triggers, holds, restrictions, or plain old technical issues.

The fastest path forward is to check for alerts, verify your information, and contact your issuer when neededbecause the issuer can see what the checkout screen won’t tell you.

And if you ever find yourself whispering, “I swear I have money,” remember: the payment system isn’t judging your life choices.

It’s just enforcing rules, preventing fraud, and occasionally throwing a tantrum like a printer that senses fear.

Common Experiences: “Yep, That Happened to Me” (Real-World Scenarios)

People don’t usually tell stories about the time their card worked perfectly. They tell stories about declinesbecause declines are dramatic, inconvenient, and weirdly memorable.

Here are a few common, very realistic experiences that pop up again and again, along with what typically fixes them.

The “I’m Literally Holding the Card” Online Decline

Someone tries to buy something onlinemaybe a gift, maybe concert tickets, maybe a last-minute airline seat upgradeand the website says the payment was declined.

They try again. Declined. They try a third time because hope is powerful. Declined again.

Then they walk into a store and the card works instantly, which makes the whole situation feel personal.

What’s usually happening: the online purchase triggers extra verification checks (billing address and ZIP, CVV, or merchant fraud filters).

The fix is often surprisingly small: entering the billing address exactly as the bank has it (including abbreviations),

updating an old address on file, or confirming the purchase in a bank alert.

Occasionally, the merchant’s system flags the order because it’s a first-time buyer, a high-dollar cart, or an unusual shipping address.

The Gas Pump That Requests “A Little Hold” (But “A Little” Means $150)

A classic: someone has enough money for gas, but the pump declines their card. They try another pump. Declined.

They start questioning reality. They check their appthere’s plenty of room for the actual purchaseso why the decline?

What’s usually happening: the pump places a preauthorization hold that can be much higher than the final amount.

If available credit is tight, that hold can fail even when the final purchase would have been fine.

The fix is to pay inside, prepay a specific amount, or use a different card with more available credit.

(Also: it’s a good reminder that “available credit” is not always the same as “what the pump wants right now.”)

The Travel Decline That Hits at the Worst Possible Time

People often discover travel-related declines at the precise moment they need the card mosthotel check-in, car rental counter, airport kiosk, or a dinner bill with eight people staring politely into their napkins.

The decline feels dramatic, but it’s commonly just a fraud-prevention tripwire: new location, new merchant category, unusual purchase size, or a charge that looks inconsistent with your normal pattern.

Typical fix: respond to the issuer alert (text/app), call the issuer to confirm you’re traveling, or try again after verification.

Lots of travelers learn the “backup method” lesson the hard way and start keeping a second card or a digital wallet option for emergencies.

The Subscription Decline That Quietly Wrecks Your Day

This one is sneaky: the card decline doesn’t happen in publicit happens silently in the background.

A streaming service, cloud storage plan, or app subscription can’t charge your card, and suddenly you’re locked out… at exactly the wrong time.

People often don’t realize their card was replaced, expired, locked, or maxed out until the subscription fails.

Fix: update payment info, confirm the card is active, and check whether the card is temporarily locked in the issuer app.

Sometimes a quick payment toward the balance restores available credit enough for the subscription to go through on the next attempt.

The “It Worked Everywhere Else” Mystery Decline

Someone buys groceries, gets coffee, pays a billeverything works. Then one specific merchant declines the card repeatedly.

That’s when the theories start: “My bank hates this store,” “The universe is sending a message,” “I’m cursed.”

Often it’s not that deep. It can be a terminal issue, a temporary network outage, a processing configuration problem, or a merchant system that’s struggling.

The fix might be as simple as trying another register, using tap instead of chip, or waiting a few minutes and retrying once.

If it keeps happening, the issuer can tell you whether they’re even receiving a valid authorization request from that merchant.

The takeaway from all these experiences is surprisingly comforting: most declines have a boring explanation and a practical solution.

And once you’ve been declined once or twice, you learn the true adult skill: calmly switching payment methods while pretending this is all very normal.