Table of Contents >> Show >> Hide

- What a “Pay for Delete” Letter Is (and What It Isn’t)

- Does Pay for Delete Work? The Realistic Answer

- Before You Send a Pay for Delete Letter: A Smart Checklist

- 1) Pull your credit reports (the right way)

- 2) Confirm who owns the debt

- 3) Check for errors (don’t negotiate with bad data)

- 4) Consider debt validation (especially if this is new to you)

- 5) Decide your offer (full pay vs. settlement)

- 6) Protect your payment method

- 7) Get the agreement in writing before you pay

- Sample Pay for Delete Letter Template (Copy-and-Use)

- What to Include (and What to Avoid) in a Pay for Delete Letter

- After You Send It: A Simple Follow-Up Timeline

- If They Refuse: Alternatives for Credit Report Cleanup

- FAQ: Quick Answers People Google at 2:00 AM

- Real-World Experiences: What People Commonly Run Into (Extra Insights)

- Experience #1: “They said yes… but only after I made it easy for them.”

- Experience #2: “I paid first and suddenly nobody remembered our ‘agreement.’”

- Experience #3: “The collector deleted their line, but the charge-off stayed.”

- Experience #4: “They offered a compromise: update to paid, no deletion.”

- Experience #5: “Disputes worked faster than negotiatingbecause the data was wrong.”

- Experience #6: “The best ‘cleanup’ was a plan: pay, document, monitor, repeat.”

- Conclusion: Clean Up Your Credit Report the Smart Way

If your credit report were a bedroom, a collection account is the random sock that somehow

keeps reappearing no matter how many times you “clean.” The good news: you may have options.

One of the most talked-about (and most misunderstood) tools is the pay for delete letter

a negotiation request asking a collection agency to remove a collection tradeline from your credit reports

in exchange for payment.

This guide gives you a sample pay for delete letter template, explains when it can help,

how to avoid common mistakes, and what to do if the collector says “nice try.” We’ll keep it practical,

compliant, and just funny enough to keep your eyeballs from filing their own dispute.

What a “Pay for Delete” Letter Is (and What It Isn’t)

A pay for delete request is exactly what it sounds like: you offer to pay (in full or settle)

and ask the debt collector to delete the collection entry from your credit reports.

The goal is credit report cleanupremoving a negative item so your report looks healthier

to lenders, landlords, and sometimes even employers.

It isn’t a magic eraser for accurate information

Credit reporting rules are built around accuracy. If a collection is legitimate and reported correctly,

it may remain on your report for years even after you pay. Pay-for-delete is a negotiation tactic,

not a guaranteed right.

Pay for delete vs. disputing vs. goodwill letters

-

Disputing: If the item is inaccurate, incomplete, or can’t be verified, you can dispute it.

If it can’t be verified, it must be removed or corrected. - Goodwill letter: Typically used for late payments with original creditors when you’ve otherwise been a good customer.

- Pay for delete: Usually aimed at third-party collectors or debt buyers for collection tradelines.

Does Pay for Delete Work? The Realistic Answer

Sometimes. Some collectors will do it, some won’t, and some will only do it under specific conditions.

It’s also worth knowing that pay-for-delete has been widely described as conflicting with certain industry

furnishing policiesone reason collectors may refuse even if they’re allowed to negotiate settlements.

Why collectors often say “no”

- Policy: They may say they must report accurately and consistently.

- Process: They might not have a deletion workflow (or they don’t want one).

- Leverage: If they think you’ll pay anyway, they may not offer extras.

When it can actually help your credit score

Here’s the tricky part: credit scoring models don’t all treat collections the same.

Some newer models may ignore certain paid collections, while older models can still count them.

That’s why deletion can be more powerful than simply “paid” statusespecially if you’re preparing for

a major loan where older scoring models may still show collections as a drag.

Translation: paying is good; paying with a deletion agreement can be even betterbut only if the deletion

actually happens.

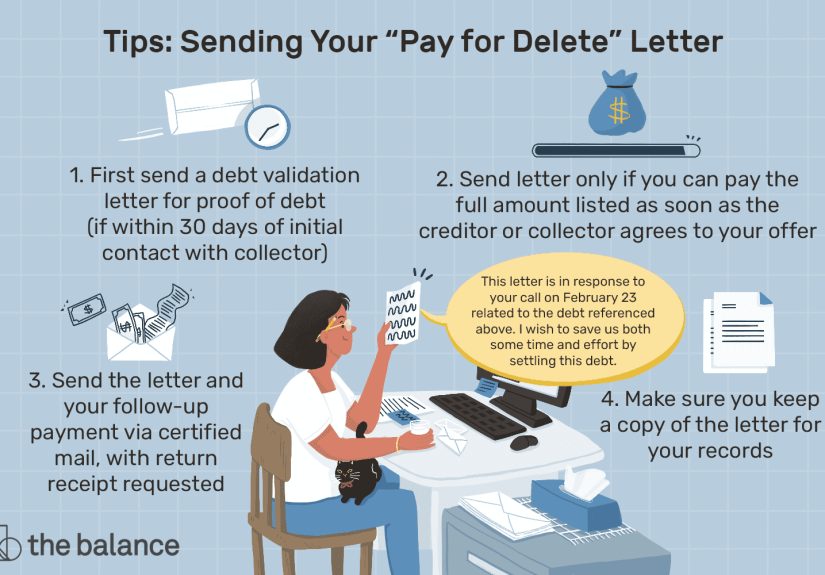

Before You Send a Pay for Delete Letter: A Smart Checklist

A strong pay for delete letter starts before you write it. Use this checklist to avoid paying the wrong

collector, reviving an old debt, or accidentally agreeing to something you didn’t mean to.

1) Pull your credit reports (the right way)

Get your reports from all three bureaus so you know exactly what’s being reported, by whom, and where.

Review the account details: dates, amounts, creditor name, collector name, and any notes about disputes.

2) Confirm who owns the debt

Sometimes the original creditor still owns the debt and hired a collection agency; other times the debt

was sold to a debt buyer. Your negotiation approach can change depending on who has authority to update

or delete reporting.

3) Check for errors (don’t negotiate with bad data)

If the collection is wrongwrong amount, wrong person, wrong dates, duplicated, or already paidyour first

move may be a dispute, not a deal. Pay-for-delete is best for debts that are likely valid, where your main goal

is improving your credit report presentation.

4) Consider debt validation (especially if this is new to you)

If a collector is contacting you and you’re unsure the debt is yours, you can request validation information.

Don’t pay a debt you can’t clearly identify.

5) Decide your offer (full pay vs. settlement)

- Pay in full: Stronger offer; may improve odds of a deletion agreement.

- Settlement: You pay less; deletion becomes less likely, but not impossible.

6) Protect your payment method

Avoid giving direct access to your bank account. Use a method you can document. Keep records of everything:

letters, emails, payment confirmation, and any agreement.

7) Get the agreement in writing before you pay

This is the single most important rule. If you pay first, your leverage often disappears faster than a cookie

at a school lunch table.

Sample Pay for Delete Letter Template (Copy-and-Use)

Below are two versions: (1) pay in full and (2) settlement. Use only the parts that fit your situation.

Keep the tone polite and simple. You are negotiatingno threats, no drama, no 12-paragraph memoir about

how this collection ruined your vibe.

Version A: Pay in Full for Deletion

Version B: Settlement Amount for Deletion

What to Include (and What to Avoid) in a Pay for Delete Letter

Include

- Correct account/reference number and original creditor name

- Your specific offer amount and how quickly you’ll pay after written acceptance

- A clear request to delete from all three bureaus

- Simple “in writing first” boundary

- Professional, calm tone (polite works better than spicy)

Avoid

- Admitting facts you’re unsure about (“I definitely owe this” if you’re not 100% sure)

- Long emotional stories (save those for your group chat)

- Threats (“Delete it or else…”)that’s not negotiation, that’s noise

- Sending payment before you have a written agreement

- Assuming they must deletethey don’t have to agree

After You Send It: A Simple Follow-Up Timeline

- Day 1: Send the letter and keep a copy for your records.

- Day 7–14: If no response, call and ask for the status (keep notes: date, time, rep name).

- When accepted: Get the agreement in writing, then pay exactly as agreed.

- 30–60 days after payment: Pull updated reports and confirm deletion happened.

- If not deleted: Contact the agency with the agreement and payment proof.

If They Refuse: Alternatives for Credit Report Cleanup

If the collector won’t delete, you still have options that can helpsometimes more reliably than pay-for-delete.

1) Dispute inaccurate or unverified information

If something is incorrect or can’t be verified, dispute it with the credit bureaus and (when appropriate)

the furnisher. Accuracy is the foundation of credit reporting. If the information can’t be verified after

a dispute, it may need to be removed or corrected.

2) Negotiate for “paid” status and stop further damage

Even if a collection stays, updating it to “paid” or “settled” can be better than leaving it open and unpaid.

Also, resolved collections can reduce the risk of escalation (like a lawsuit), depending on your situation.

3) Try a goodwill approach (when it fits)

Goodwill letters are better suited to original creditors (like a credit card issuer) when you had a one-time

slip and you’re otherwise in good standing. They’re not guaranteed, but they’re low-risk and sometimes effective.

4) Build positive credit history around the negative

Credit scores weigh more than “bad stuff.” On-time payments, low utilization, and time can steadily offset old damage.

Think of it like adding good reviews to drown out one weird review that says your restaurant “has vibes.”

FAQ: Quick Answers People Google at 2:00 AM

Will a paid collection automatically disappear?

Usually, no. It may remain for the standard reporting period, but it should update to show it’s paid.

Should I send a pay for delete letter to the original creditor?

You can try, but pay-for-delete is more commonly negotiated with third-party collectors. Original creditors may be less willing

to remove accurate history.

Is a pay for delete letter “legal”?

It’s generally a private negotiation request, but it’s not guaranteed and can be controversial. Always keep your communications truthful,

and never ask anyone to report inaccurate information.

What if the collector agrees by phone but won’t put it in writing?

Then treat it as a “no.” If it’s not in writing, it’s not a deal.

Real-World Experiences: What People Commonly Run Into (Extra Insights)

I don’t have personal life experiences, but here are patterns that consumers commonly report when trying pay-for-delete

presented as realistic scenarios so you can recognize them in the wild.

Experience #1: “They said yes… but only after I made it easy for them.”

A lot of people start with a vague letter like, “Please remove this.” The responses are equally vague: “We report accurately.”

The folks who report better results tend to do two things: (1) they make a specific offer (“$___ within ___ days”), and

(2) they keep the request simple (“delete the collection tradeline from all three bureaus after payment”).

It’s not about being fancyit’s about being clear. Collectors process hundreds (or thousands) of accounts. Your letter needs

to be readable in one pass, like a drive-thru order.

Experience #2: “I paid first and suddenly nobody remembered our ‘agreement.’”

This one shows up often: someone calls, hears “we can take care of it,” pays immediately, and later learns the tradeline is still there.

The takeaway isn’t that every collector is shadyit’s that call-center conversations are hard to prove and easier to misunderstand.

People who protect themselves tend to insist on a written agreement before paying. If a collector truly plans to delete,

putting it in writing shouldn’t be a dealbreaker. If it is a dealbreaker, that tells you something.

Experience #3: “The collector deleted their line, but the charge-off stayed.”

Another common surprise: the collection agency deletes their collection entry, but the original creditor’s charge-off

(or late-payment history) remains. That’s not necessarily a failurecollections and charge-offs can be separate tradelines.

When consumers expect “everything disappears,” they’re often disappointed. A smarter expectation is:

“Can I remove the collection entry?” and separately, “Is the original creditor reporting accurate information?”

This is why it helps to review all tradelines tied to the same debt before negotiating.

Experience #4: “They offered a compromise: update to paid, no deletion.”

Many people report the collector offered a middle ground: “We’ll mark it paid in full” or “settled,” but won’t delete.

This isn’t worthless. Depending on the scoring model used, “paid” can help a little, help a lot, or help not at all.

But in real-life lending decisions, a paid collection can look better than an unpaid one. Some consumers accept the compromise,

then focus on adding positive credit history to speed up recovery.

Experience #5: “Disputes worked faster than negotiatingbecause the data was wrong.”

People sometimes chase pay-for-delete when the simpler move was disputing an error. Common mistakes include:

wrong balance, wrong dates, duplicated collections, or accounts that belong to someone else (identity mix-ups happen).

When documentation doesn’t match, disputes can lead to correction or removal. The practical lesson:

always check accuracy first. Negotiate second.

Experience #6: “The best ‘cleanup’ was a plan: pay, document, monitor, repeat.”

The most consistent wins tend to come from a boring-but-effective system:

pull all three reports, list every negative item, prioritize by impact and urgency, document every action,

and re-check reports on a schedule. It’s not glamorous. It’s also how you avoid paying the wrong collector,

missing a response letter, or forgetting to verify whether the tradeline actually changed. Credit repair, done responsibly,

looks less like a dramatic movie montage and more like a tidy spreadsheet.

Conclusion: Clean Up Your Credit Report the Smart Way

A sample pay for delete letter can be a useful tool for credit report cleanup,

but it works best when you treat it like a negotiation: verify the debt, make a clear offer, insist on written terms,

and keep impeccable records. If the collector refuses, you can still improve your credit profile by disputing inaccuracies,

resolving the balance, and building strong positive credit habits around any old negatives.

Most importantly: don’t ask anyone to report false information, and don’t rely on verbal promises. Your future self

will thank youand might even stop doom-scrolling credit forums at midnight.