Table of Contents >> Show >> Hide

- What Does “VC Returns” Even Mean?

- So Why Are VC Returns at a 10+ Year Low?

- PitchBook Signals: The Story Behind “Paper Returns”

- Fundraising Didn’t CollapseIt Concentrated

- The Exit Reality Check: IPOs, M&A, and Timing

- Why AI Didn’t Automatically Fix VC Returns

- What Founders Should Do When VC Returns Are Low

- What LPs and GPs Can Do: Managing the “Wait”

- Is “10+ Year Low” a Warning Sign or an Opportunity?

- Quick Glossary: VC Return Terms You’ll Hear in Every Meeting

- Conclusion: What to Take Away from PitchBook’s “Low Returns” Moment

- Added Experiences and Real-World Patterns When VC Returns Hit Multi-Year Lows (500+ Words)

- Experience Pattern #1: The Diligence Questions Change Overnight

- Experience Pattern #2: Down Rounds Become Strategy, Not Shame

- Experience Pattern #3: “Exit Optionality” Becomes a Product Requirement

- Experience Pattern #4: The Best Companies Start Acting Like Grown-Ups

- Experience Pattern #5: Everyone Suddenly Cares About DPI

Venture capital has always been a little weird. It’s an asset class where patience is a strategy, spreadsheets are a love language,

and “we’ll know in 10 years” is considered a totally normal timeline. So when PitchBook-themed headlines start floating around that

VC returns are at a 10+ year low, it lands like a cold splash of reality on a warm bubble bath.

But here’s the twist: low returns don’t necessarily mean “venture is broken.” They often mean “venture is between chapters.”

The 2020–2021 era rewarded growth-at-all-costs. The post-rate-hike era is grading everyone on fundamentals and liquidity.

And liquidity, lately, has been playing hide-and-seek with the enthusiasm of a toddler who thinks they’re invisible.

In this deep dive, we’ll unpack what “10+ year low” can mean in VC, why returns have been squeezed, what metrics matter (IRR, DPI, TVPI),

and what founders and investors can do when the music slows down and nobody wants to be the last one holding illiquid chairs.

What Does “VC Returns” Even Mean?

Before we declare venture capital “down bad,” we need to define returnsbecause VC returns can look very different depending on

when you measure them and how you measure them.

The 3 Metrics That Rule Venture Returns

-

IRR (Internal Rate of Return): A time-weighted annualized return estimate. Useful, but it can be distorted by

early markups, write-downs, and the “one big exit” effect. -

DPI (Distributions to Paid-In): The cash actually returned to investors divided by the cash invested. This is the

“show me the money” metric. -

TVPI (Total Value to Paid-In): DPI plus the remaining unrealized value. This includes both realized cash and

paper valueso it can look great right until it doesn’t.

In good times, TVPI rises quickly because private valuations climb and follow-on rounds happen at higher prices. In tougher times,

the market cares less about paper wins and more about cash winswhich is why DPI becomes the star of the show.

And right now, that show is on a delayed release schedule.

So Why Are VC Returns at a 10+ Year Low?

There isn’t one villain here. It’s more like a heist movie where multiple things go wrong at once and everyone keeps whispering,

“This wasn’t in the plan.”

1) Exit Markets Have Been the Blockade

Venture returns don’t materialize because companies are “promising.” They materialize because companies exit.

If exits slow, distributions slow. If distributions slow, LPs get grumpy. If LPs get grumpy, fundraising gets weird.

And fundraising being weird is practically the official sport of 2024–2025.

Industry monitoring has pointed out that the number of return-generating, large exits has been limited even when overall exit counts

look “okay,” because many exits have been smaller and less capable of moving the needle for fund-level outcomes.

In other words: lots of activity, not enough fireworks.

2) Higher Rates Repriced Growth (and Patience)

When rates rise, discount rates rise. That makes future cash flows worth less today. Growth multiples compress.

Late-stage venture feels it first, but the ripple eventually hits earlier rounds tooespecially when founders need follow-on capital

in a market that’s suddenly allergic to “narrative-only” valuations.

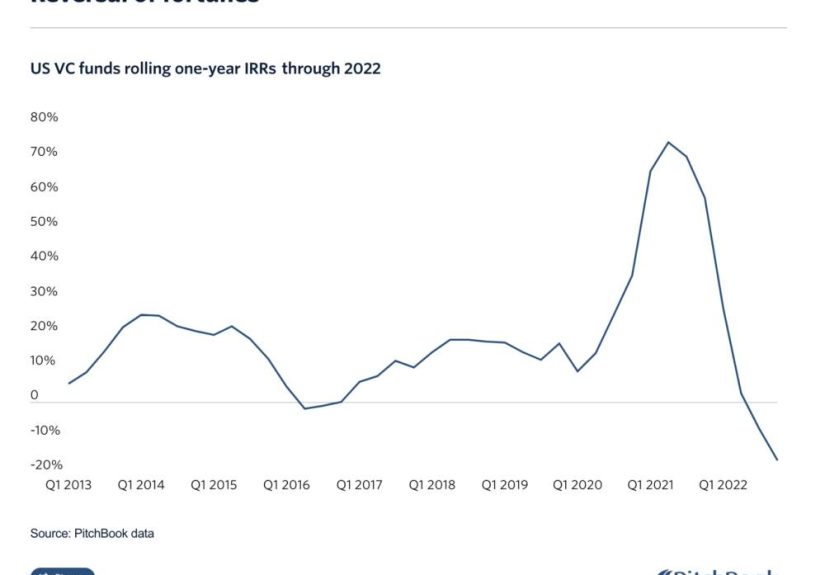

This is one reason “paper returns” can drop sharply: the market re-rates comparable public comps, and private marks have to acknowledge

reality. PitchBook performance commentary has shown rolling return measures can fall meaningfully during these cycles, including periods

where VC rolling one-year IRR sank to levels not seen in years. That’s the math version of “gravity still works.”

3) The Liquidity Squeeze Changed LP Behavior

Limited partners (pensions, endowments, family offices, and the like) don’t just invest in VC; they manage portfolio targets.

When public markets move sharply and private assets don’t reprice as fast, allocations can get out of whack (often called the

“denominator effect”). The result is less appetite for new commitmentsespecially when distributions are thin.

The consequence: even when VC investment opportunities exist, fundraising can stay muted until more value turns into cash.

“Paper” doesn’t pay for next year’s commitments.

4) Returns Became Highly Concentrated

Even in better environments, venture returns are famously “power-law.” A small slice of deals drives most of the outcomes.

In a tougher environment, that concentration becomes more extreme:

- Fewer mega-exits means fewer “fund makers.”

- More flat/down exits means returns get capped.

- More capital chasing fewer obvious winners means pricing pressure stays intense at the topwhile everything else struggles.

This helps explain the awkward combo we’ve seen: massive excitement in a few areas (hello, AI) while fund-level returns still look muted

because liquidity hasn’t caught up.

PitchBook Signals: The Story Behind “Paper Returns”

When you see commentary about “paper returns” being down, it usually refers to mark-to-market changes in portfolio valuebefore those

values become cash via exits. During the 2022 reset, PitchBook performance reporting showed rolling VC IRR measures dropping sharply from

2021 highs, and quarterly returns turning negative for stretches. That’s the kind of environment that can set up “multi-year lows.”

SaaStr’s PitchBook-flavored takeawayframed as a “10+ year low” momentcaptures the emotional truth founders and investors felt in the

downturn: marks fell, optimism cooled, and a lot of decks quietly replaced “hypergrowth” with “operating leverage.”

Same PowerPoint template, very different vibe.

Fundraising Didn’t CollapseIt Concentrated

One of the most important shifts isn’t just “less money.” It’s money flowing to fewer firms.

Venture monitoring highlighted a year where fundraising totals remained meaningful, but fund counts were at decade lowsand

capital clustered around brand-name managers.

Why This Matters for Returns

- Emerging managers face tougher fundraising, which can reduce diversification across the ecosystem.

- Top-tier firms may still do well, but broader industry averages can look weak when many funds are stuck waiting for exits.

- Selection risk increases for LPs: picking the wrong managers in a low-liquidity era can be painful for a long time.

In plain English: the venture “middle class” got squeezed, and that changes the shape of future returns.

The Exit Reality Check: IPOs, M&A, and Timing

Venture capital is supposed to be illiquid, but not “perpetually pending.” When the IPO window narrows and large acquisitions slow,

time-to-liquidity stretches.

Legal-market reporting on the US VC ecosystem has pointed out that IPO outcomes in weaker periods can be rough on investors and that M&A

often becomes the preferred liquidity path when public listings are scarcebecause cash at close beats “we’ll sell after lockup if markets feel cute.”

This is also where return math gets unforgiving. A decent multiple earned quickly can beat a bigger multiple earned slowly.

Timing isn’t just a detail in VC; it’s the hidden boss level.

Why AI Didn’t Automatically Fix VC Returns

If you only looked at headlines, you might think AI “revived” venture. And it didpartially.

PitchBook-based reporting showed AI capturing a huge share of US VC dollars, with overall funding up year-over-year in 2024.

But funding volume is not the same thing as fund performance.

Returns require exits. And even when AI dealflow is strong, large-scale liquidity events can lag by years.

Meanwhile, big AI rounds can concentrate value in a smaller number of companiesgreat if you’re in them, less great if your fund isn’t.

What Founders Should Do When VC Returns Are Low

Low-return eras change investor behavior. The fastest way to understand the new market is to listen to what diligence asks for.

When returns are scarce, investors become allergic to avoidable risk.

Founder Playbook for a Low-Return VC Cycle

- Build a longer runway: Raise enough to hit undeniable milestones, not just “stay alive.”

- Make margins a product feature: If you can improve gross margin, retention, or payback, highlight it loudly.

- Tell a cash story, not only a growth story: Show how the business becomes self-sustaining over time.

- Expect more structure: Protective terms and valuation discipline show up more often in tough cycles.

- Plan for multiple exit paths: Strategic M&A readiness matters when IPOs are selective.

The good news: companies built in disciplined markets often become the strongest stories when the cycle turns.

The bad news: disciplined markets demand discipline. (Shocking, I know.)

What LPs and GPs Can Do: Managing the “Wait”

When distributions lag, everyone starts optimizing for liquidity. That means secondaries, continuation vehicles, and

more creative fund structures get attention. But even without financial engineering, there are practical moves.

For LPs

- Re-underwrite pacing: Commitments made in boom years may require a slower plan until cash flows normalize.

- Stress-test liquidity: Model capital calls under multiple scenarios, including “exits stay slow.”

- Manager selection becomes everything: In a power-law class, access and discipline matter more in downturns.

For GPs

- Be transparent about marks: LP trust is currency when cash is scarce.

- Support portfolio durability: Extensions, bridge rounds, and strategic help can prevent value-destroying outcomes.

- Think about liquidity tools early: If a company can exit modestly now vs. maybe later, at least run the math.

Is “10+ Year Low” a Warning Sign or an Opportunity?

Both. Low-return periods are uncomfortable, but they also reset expectations, valuations, and behavior in ways that can improve forward returns.

When prices normalize and deal terms become investor-friendly, new vintages can benefitespecially if exit markets reopen within a reasonable window.

The key is not confusing “low recent returns” with “no future returns.” Venture is cyclical. The industry has down years, then rebounds.

Benchmark commentary has shown VC performance can recover after drawdownseven if the path is uneven and concentrated.

Quick Glossary: VC Return Terms You’ll Hear in Every Meeting

- Paper returns: Unrealized value changes based on marks; not cash.

- Realized returns: Cash back from exits or distributions.

- Vintage year: The year a fund starts deploying capital; critical for comparing peers fairly.

- Dry powder: Capital committed but not yet invested; grows when fundraising stays high but deployment slows.

- Down round: A financing at a lower valuation than the prior round; can reset incentives and cap tables.

Conclusion: What to Take Away from PitchBook’s “Low Returns” Moment

“VC returns are at a 10+ year low” is less a tombstone and more a weather report. The environment shifted:

exits slowed, rates rose, marks fell, and LP liquidity became precious. That combination pulls down recent performance and makes fundraising harder,

especially for newer managers.

But it also forces the ecosystem to do what it claims to do: fund durable innovation, build real businesses, and earn returns through exitsnot vibes.

If liquidity improves and the exit market reopens meaningfully, the next chapter can look very different.

Until then, the best strategy is simple (and annoyingly timeless): build quality, price risk honestly, and plan for patience.

Added Experiences and Real-World Patterns When VC Returns Hit Multi-Year Lows (500+ Words)

The word “experience” can sound like someone’s about to tell a dramatic campfire story. In venture, the campfire is usually a group chat,

and the scary part is a term sheet with more redlines than a high school English essay. What follows are composite, real-world patterns

that repeatedly show up across low-return cyclesbased on how the market tends to behave when liquidity is scarce and optimism gets a budget cut.

Experience Pattern #1: The Diligence Questions Change Overnight

In frothy markets, founders get asked, “How big can this get?” In low-return markets, they get asked, “How does this survive?”

A common pattern is that diligence shifts from vision-first to mechanics-first. Investors spend more time on:

customer concentration, net revenue retention, sales efficiency, burn multiple, and whether margins can improve without

“hoping the next round fixes it.” Founders who anticipate this shift often win time back: they answer the hard questions in the deck,

not in a surprise email thread at midnight.

Experience Pattern #2: Down Rounds Become Strategy, Not Shame

In a multi-year low environment, down rounds stop being rare and start being a tool. A down round can be painful,

but it can also reset the cap table, restore employee equity incentives, and align the valuation with real market demand.

The founders who navigate this best tend to treat the round as a restructuring moment:

they negotiate clean governance, preserve enough option pool for hiring, and communicate the “why” internally so the team

doesn’t fill the silence with worst-case assumptions. The hard lesson is that valuation is not a trophyit’s a contract with consequences.

Experience Pattern #3: “Exit Optionality” Becomes a Product Requirement

When IPOs are selective and mega-acquisitions slow, companies that look attractive to strategics gain leverage.

That usually means clear differentiation (data, workflow lock-in, platform advantage) and a story that makes sense

for a buyer’s P&L. In low-return markets, many leadership teams quietly build an acquisition narrative alongside

the standalone narrative: partnerships that could convert into M&A, integration points, and a roadmap that reduces

buyer risk. It’s not “selling out”it’s designing for multiple outcomes.

Experience Pattern #4: The Best Companies Start Acting Like Grown-Ups

Low-return markets tend to reward operational maturity earlier. The teams that stand out often tighten planning cadences,

shorten feedback loops, and build forecasting discipline. They also get serious about hiring: fewer “nice-to-have” roles,

more revenue- or product-critical roles. The cultural shift is noticeable: less dopamine-driven expansion, more

craftsmanship. Ironically, this is often when companies become healthiestbecause constraints force clarity.

Experience Pattern #5: Everyone Suddenly Cares About DPI

In boom times, conversation centers on TVPI and marks: “Look at our unrealized value!” In low-return cycles, LPs want receipts.

They ask how and when cash comes back. That changes GP behavior: more focus on liquidity planning, secondaries, structured exits,

and realistic timelines. It also changes how fundraising works: established firms with strong historical outcomes often attract a

disproportionate share of commitments, while newer managers struggle to prove themselves without a friendly exit market.

The experience many people describe is not just “capital is tighter,” but “trust is tighter.”

The most consistent takeaway from these patterns is that low-return eras don’t eliminate opportunitythey change what opportunity looks like.

They favor builders over storytellers, discipline over momentum, and cash pathways over hypothetical futures.

If that sounds less fun than the boom years, you’re not wrong. But it can produce stronger companies and, eventually, better returns

because the deals done with valuation sanity and real operating progress tend to age well when the cycle turns.