Table of Contents >> Show >> Hide

Note: This article is for educational purposes only. It uses current U.S. retirement-plan data and hypothetical growth examples, not personalized investment, tax, or legal advice.

Becoming a 401(k) millionaire sounds glamorous, like something that should involve a lake house, a suspiciously expensive watch, and at least one sentence beginning with, “My financial advisor says…” In real life, it is usually much less dramatic. Most 401(k) millionaires are built the boring way: payroll deduction by payroll deduction, year after year, with a little employer match, a lot of patience, and the emotional strength to avoid doing something spectacularly unhelpful during a market panic.

So, how hard is it to become a 401(k) millionaire? The honest answer is this: it is hard, but it is not absurd. It is difficult for the average worker to reach $1 million quickly. It is much more realistic over a full career, especially if you start early, capture your full employer match, increase contributions as your income rises, and stay invested through ugly market years. In other words, it is less like winning the lottery and more like brushing your teeth. Boring, repeated effort does the heavy lifting.

The Short Answer: Hard for a Decade, Easier Over Decades

A million dollars in a 401(k) is still a major milestone, but it is not magical. It does not automatically mean “rich,” and it definitely does not mean “I can retire tomorrow and spend every afternoon buying decorative olives.” It means you have accumulated serious retirement assets in a tax-advantaged account. Whether that is enough depends on your retirement age, spending habits, taxes, inflation, and whether you plan to live like a minimalist monk or a cruise director.

The reason the goal feels so intimidating is simple: most people are not close to it. Recent large-plan data show average 401(k) balances are far below $1 million, and median balances are much lower still. That gap matters. It tells us that millionaire status is real and achievable, but it is not typical. It usually belongs to workers who had a long time horizon, steady employment, decent income growth, employer contributions, and the discipline not to raid the account every time life got noisy.

That is why the question is not really, “Can someone become a 401(k) millionaire?” The answer to that is clearly yes. The better question is, “How much time, savings discipline, and career stability does it usually take?”

Why the Math Matters More Than Motivation

Motivation is nice. Math is nicer.

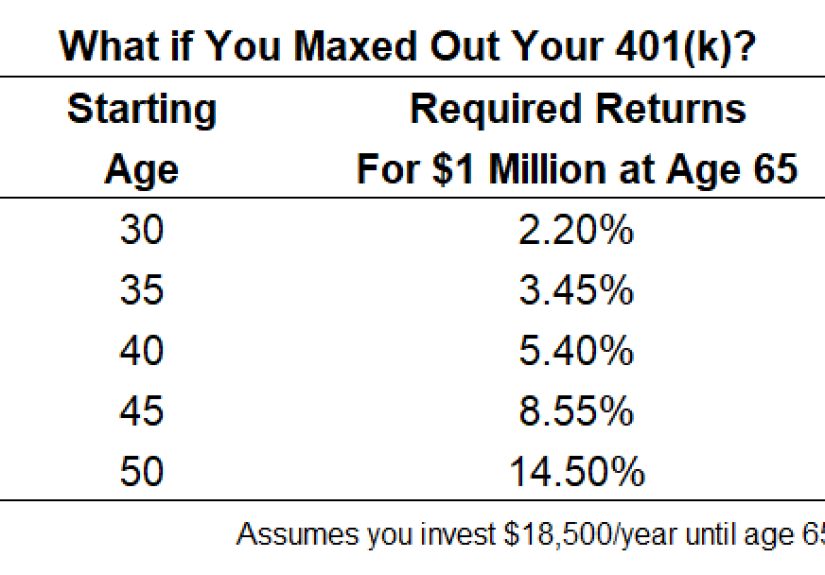

As of 2026, the IRS allows workers to defer up to $24,500 into a 401(k), with catch-up contributions available for older savers. If you are age 50 or older, the standard catch-up amount can push your total elective deferral higher, and workers ages 60 through 63 may qualify for an even bigger catch-up limit. That sounds generous on paper, but many workers are nowhere near maxing out their accounts.

And honestly, that is understandable. Based on recent full-time wage data, the median worker earns about $62,600 a year. On that income, contributing the full $24,500 would mean deferring roughly 39% of gross pay before the employer match even enters the chat. For a typical household dealing with rent, groceries, insurance, student loans, and the occasional “Why is my car making that sound?” moment, that is a brutal lift.

So here is the first big truth: most 401(k) millionaires do not get there because they maxed out from day one. Many get there because they started reasonably early and kept going.

Illustrative Example 1: The Early Starter

Let’s say a worker starts at age 25, earns $60,000, saves 10% of pay, receives a 4% employer match, gets 3% annual salary growth, and earns a hypothetical long-term 7% annual return. By age 65, that saver could end up with roughly $2.46 million.

That is the power of time. Not genius. Not secret stock picks. Not “I read one thread online and now I only invest in companies that make robot soup.” Just time and consistency.

Illustrative Example 2: The Same Saver, Ten Years Later

Now take the exact same habits and start at age 35 instead of 25. Same salary. Same savings rate. Same employer match. Same growth assumptions. The ending balance drops to about $1.09 million.

Still a millionaire? Yes. But look at what ten missing years cost. More than a million dollars in potential ending wealth vanished, and that is before we even start debating inflation.

Illustrative Example 3: Starting at 40

Start the same plan at age 40, and the ending balance falls to roughly $700,000. That is still meaningful retirement money. It is just not 401(k)-millionaire money under these assumptions.

This is why becoming a 401(k) millionaire is hard mostly because of timing, not because the math is impossible. Time is the co-worker who does half the project while saying very little.

What Makes the Goal Harder Than It Looks

1. Many workers do not have tons of margin

Retirement saving competes with every other financial goal. Housing, debt payments, family costs, emergency savings, healthcare, and day-to-day inflation all take a bite. Even when workers know they should save more, cash flow can make that difficult.

2. Not everyone has equal access to a great plan

Workplace access has improved, but it is still not universal. Some workers do not have a 401(k). Others have one with limited matching, delayed eligibility, or lower wages that make participation tough. A millionaire target is a lot easier when the employer is helping.

3. People miss free money

One of the most painful retirement mistakes is failing to contribute enough to earn the full employer match. That is not just leaving money on the table. That is leaving your future self on the table. Vanguard data show the average contribution needed to maximize a typical match is around 6% to 6.5% of pay. Yet many workers still do not hit that mark.

4. Cash-outs and job changes do damage

Workers change jobs often. When they do, some roll the money over responsibly. Others cash out small balances, pay taxes and penalties, and accidentally light their long-term compounding on fire. One early cash-out may not feel catastrophic, but repeated leaks can quietly destroy the millionaire path.

5. Fear can be expensive

401(k) millionaires are rarely the people who timed every market swing perfectly. They are more often the people who kept investing through rough periods, stayed diversified, and let the market recover. Panic-selling after a decline can turn a temporary drop into permanent damage.

6. Fees matter more than people think

Fees are not exciting. Neither is flossing. Both matter anyway. The Department of Labor has repeatedly warned workers to pay attention to plan fees and fund expenses because those costs can eat into long-term returns. A small fee difference, stretched over decades, is not small anymore.

What Makes Becoming a 401(k) Millionaire Easier

Start before you feel “ready”

Almost nobody feels fully ready to save a meaningful chunk of their paycheck. Starting early matters because compounding rewards time more than drama. Even modest contributions in your 20s and early 30s can do serious work later.

Get the full match first

If your employer matches 401(k) contributions, that is step one. Before optimizing your life into a spreadsheet sculpture, get the full match. It is the closest thing retirement planning offers to free money.

Use auto-enrollment and auto-escalation

Automatic features are a big deal. Large-plan research shows participation is dramatically higher in auto-enrollment plans than in voluntary ones. Automatic annual increases matter too. They help people save more without needing a monthly internal debate about whether adulthood is worth it.

Increase contributions with raises

A simple tactic works wonders: every time you get a raise, increase your 401(k) contribution by 1% or 2%. You will feel it less than making one giant jump later. This is often how ordinary savers become extraordinary accumulators.

Stay diversified and avoid constant tinkering

For people who do not want to manage a portfolio like a part-time hedge fund analyst, target-date funds can be useful. The Department of Labor notes that these funds automatically rebalance over time and can serve as a practical default for retirement savers. They are not magic, but they can prevent a lot of unforced errors.

Use catch-up contributions if you are behind

Workers in their 50s and early 60s have a chance to save more aggressively. Catch-up contributions do not erase a late start, but they can narrow the gap. For higher earners who spent earlier decades under-saving, these later-career years can be incredibly important.

So, How Hard Is It Really?

Here is the honest verdict:

Becoming a 401(k) millionaire is very hard if you start late, contribute inconsistently, miss the employer match, cash out after job changes, or earn modest wages without much room to save.

It is moderately hard if you begin in your 30s, save around 10% of pay, get a decent employer match, and stay the course for 30 years.

It is surprisingly realistic if you start in your 20s, steadily raise contributions, keep costs reasonable, and avoid sabotaging yourself during market downturns.

In other words, becoming a 401(k) millionaire is not easy, but it also is not reserved for surgeons, startup founders, or people who say things like “Let’s circle back after my ski trip to Zurich.” Plenty of ordinary workers can get there. The path just tends to be long, steady, and a little boring. Which, in retirement planning, is usually a compliment.

Common Experiences on the Road to a 401(k) Million

The experience of building a seven-figure 401(k) is rarely dramatic. More often, it feels slow, uneven, and almost weirdly unimpressive while it is happening. Many savers spend years staring at balances that seem to move like cold maple syrup. The first $10,000 can feel hard. The first $100,000 can feel harder than it should. Then, somewhere later, compounding starts acting like it finally had its coffee.

One very common experience is the late realization phase. A worker in their late 20s or early 30s finally looks at their account and realizes they have been contributing just enough to be technically responsible, but not enough to build meaningful long-term wealth. Nothing catastrophic happened. They were just on autopilot at 3% or 4%, telling themselves they would “fix it later.” Then later arrived wearing work shoes and carrying a mortgage statement. The good news is that many people recover from this stage by increasing contributions one point at a time.

Another common experience is the match wake-up call. Someone learns, often from a more financially savvy co-worker, that they have been missing part of their employer match for years. This is the retirement equivalent of discovering you left coupons on the counter, except the coupons were worth thousands of dollars and had decades to compound. For many future 401(k) millionaires, the turning point is not a giant salary jump. It is simply deciding to stop missing matched contributions.

Then there is the bear market stomach test. Almost every long-term saver hits a period where the balance drops and motivation gets punched in the face. Contributions continue, but the statement looks rude. This phase is emotionally hard because saving into a falling market feels like putting water into a bucket that keeps shrinking. Yet this is also where many successful savers separate themselves. They keep going. They remember that bad markets are temporary, but panic decisions can last forever.

A fourth experience is the raise-and-ratchet effect. This one is delightfully unsexy. A worker gets a raise, increases the 401(k) contribution by 1%, and moves on with life. Then they do it again next year. And maybe again after a promotion. Ten years later, they look up and realize they are saving at a level that once sounded impossible. This is how real progress often feels: almost invisible in the moment, obvious only in hindsight.

Finally, many savers discover the oddly comforting truth that millionaire status often arrives without fireworks. There is no parade. No eagle lands on your mailbox. You log in one day, see two commas in the balance, and think, “Huh. Well, that’s neat.” The moment is quiet because the journey was quiet. That may be the most important experience of all: retirement wealth is usually built through ordinary habits repeated long enough to become extraordinary.

Final Thought

If you are wondering whether becoming a 401(k) millionaire is hard, the answer is yes. But the better answer is that it is usually hard in a very ordinary way. It asks for time, consistency, and restraint more than brilliance. It asks you to keep saving when the account seems small, keep investing when markets are ugly, and keep increasing contributions before lifestyle inflation eats every raise alive.

That may not be flashy, but it is encouraging. Flashy is hard to repeat. Ordinary is exactly what you can build on.