Table of Contents >> Show >> Hide

- What Is a Line of Credit?

- How a Line of Credit Works Step by Step

- Draw Period vs. Repayment Period

- Types of Lines of Credit

- Line of Credit vs. Credit Card

- Line of Credit vs. Personal Loan

- How a Line of Credit Affects Your Credit Score

- When a Line of Credit Makes Sense

- When a Line of Credit Can Be a Bad Idea

- What to Check Before You Apply

- Real-World Experiences With How a Line of Credit Works

- Final Thoughts

A line of credit is one of those financial tools people hear about, nod politely at, and then secretly file under “I’ll figure it out when adulthood gets louder.” Fair enough. Between credit cards, personal loans, HELOCs, and business financing, the borrowing world can feel like a buffet where every dish looks similar until one bites back.

Here’s the simple version: a line of credit gives you access to money up to a set limit, and you borrow only what you need, when you need it. You repay what you use, and as you pay it down, that money usually becomes available again. It is flexible, reusable, and handy for expenses that do not arrive all at once with a neat little bow on top.

That flexibility is exactly why so many people search for terms like how a line of credit works, personal line of credit, HELOC vs personal loan, and line of credit vs credit card. The catch is that flexibility can be helpful or hazardous, depending on how well you understand the rules. Let’s walk through what a line of credit is, how interest works, when it makes sense, and when it can quietly turn into a budget gremlin.

What Is a Line of Credit?

A line of credit is a form of revolving credit. A lender approves you for a maximum borrowing amount, called your credit limit. You do not receive the entire amount in one lump sum. Instead, you draw funds as needed. If your limit is $15,000 and you use $2,000, you typically pay interest only on that $2,000, not the full $15,000.

That is the main appeal. A line of credit is built for uncertainty. Maybe you are paying for a home repair and do not know the final cost. Maybe you are self-employed and your cash flow behaves like a cat: independent, unpredictable, and rarely interested in your schedule. Maybe you want emergency access to funds without taking out a full loan before you need it.

Unlike an installment loan, which gives you a fixed lump sum and fixed repayment schedule, a line of credit lets you borrow in smaller chunks over time. Unlike a credit card, a personal line of credit may offer a higher borrowing limit or a lower rate, but it may also come with draw fees, variable rates, and no rewards. In other words, it is less flashy than a credit card, but sometimes more useful when real life starts sending invoices.

How a Line of Credit Works Step by Step

1. You apply and get approved for a credit limit

When you apply, the lender reviews your credit history, income, existing debts, and overall financial profile. If approved, you receive a borrowing limit. That limit could be modest for an unsecured personal line of credit or much larger for a secured option like a home equity line of credit.

Your credit limit is not random. It reflects how much risk the lender thinks you represent. Strong credit, stable income, and lower existing debt generally improve your odds of approval and better terms. Weak credit or shaky income can lead to higher rates, lower limits, or a denial that arrives with all the charm of a parking ticket.

2. You draw funds only when needed

Once the account is open, you can access money through bank transfers, checks, online withdrawals, or other methods allowed by the lender. You can borrow a little, repay a little, borrow again, and repeat the cycle as long as the account remains in its draw period and in good standing.

This is why a line of credit works well for ongoing costs. If you need money in stages rather than all at once, a revolving structure can be more efficient than borrowing a big lump sum up front and paying interest on money still sitting untouched.

3. Interest is charged on what you use

Most lines of credit charge interest only on the outstanding balance. That sounds wonderful, and it can be. But many lines of credit also have variable interest rates, meaning the rate can move up or down over time. When rates rise, your payments can become less predictable. Your line of credit may start as a helpful backup plan and slowly morph into a monthly math problem.

Some lenders also charge annual fees, maintenance fees, late fees, or draw fees each time you access the account. That means the true cost is not just the interest rate. You also need to look at the APR, fee schedule, repayment rules, and whether the lender has special conditions for keeping the account open.

4. You make monthly payments

Like a credit card, a line of credit usually requires at least a minimum monthly payment. That payment may include interest only, interest plus some principal, or a formula based on your balance. Because the balance can change month to month, your payment can change too.

This is where people get tripped up. A minimum payment is not a magic trick. It is simply the smallest amount required to keep the account current. If you make only minimum payments for too long, interest can pile up and repayment can drag on like a road trip with no snacks and three wrong exits.

5. As you repay, credit becomes available again

With revolving credit, repayment restores available borrowing capacity during the draw period. If your limit is $10,000 and you owe $4,000, you may have $6,000 available. If you repay $1,500, your available credit may go back up to $7,500. That reusable structure is what makes a line of credit so flexible and so tempting.

Draw Period vs. Repayment Period

Many lines of credit have two phases: the draw period and the repayment period. During the draw period, you can borrow, repay, and borrow again. After that phase ends, the line may close to new borrowing and shift into repayment mode.

For a personal line of credit, the draw period may last a few years, depending on the lender. For a HELOC, a common structure is a draw period of about 10 years followed by a repayment period that can last much longer. During repayment, you may no longer be able to take new draws, and your payment may increase because you are now paying principal and interest on the remaining balance.

This transition catches some borrowers off guard. They get comfortable with lower payments during the draw period and then meet the repayment phase like it is an uninvited guest carrying a larger bill.

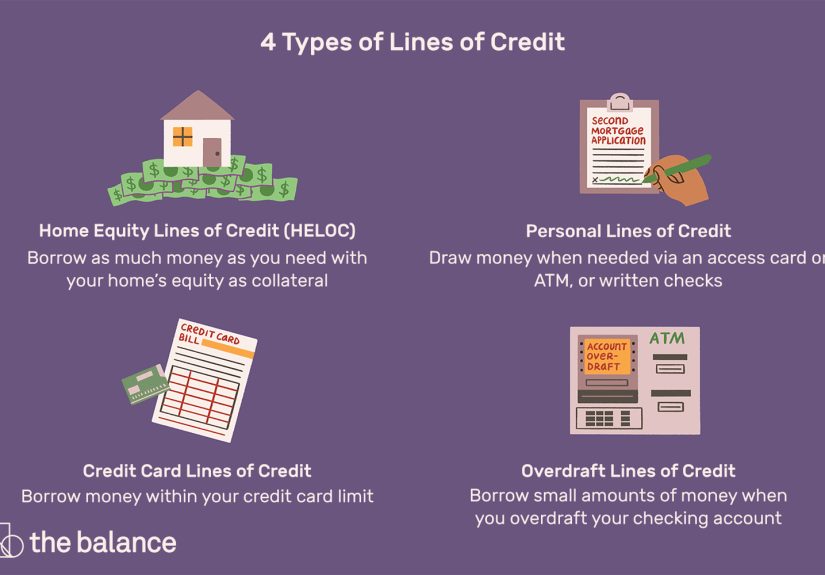

Types of Lines of Credit

Personal line of credit

A personal line of credit is usually unsecured, meaning it does not require collateral. Approval depends heavily on your credit profile and income. It is commonly used for emergency expenses, medical bills, home projects, weddings, or debt management when costs are spread over time.

Home equity line of credit (HELOC)

A HELOC is secured by your home. You borrow against your available home equity, which often means lower rates than unsecured borrowing. The tradeoff is obvious and serious: your home is on the line. A HELOC can make sense for major renovations or large expenses, but it should never be treated like free money with nicer packaging.

Business line of credit

A business line of credit helps businesses handle short-term working capital needs, inventory purchases, payroll gaps, seasonal swings, or uneven receivables. It is often used for cash flow management rather than long-term investment. Think of it as a financial shock absorber, not a magic fountain.

Secured vs. unsecured

Some lines of credit are secured by collateral, while others are unsecured. Secured credit lines may offer larger limits or lower rates because the lender has added protection. Unsecured lines usually rely on your creditworthiness alone, which can mean stricter approval standards or higher rates.

Line of Credit vs. Credit Card

This comparison confuses people because both are revolving credit. Both have limits. Both let you borrow and repay repeatedly. Both can affect your credit score through payment history and utilization.

But they are not twins. A credit card is built for purchases and often comes with rewards, statement cycles, and a grace period on purchases if you pay in full on time. A personal line of credit may not offer rewards, may start charging interest from the moment you draw funds, and may include transaction or maintenance fees. On the flip side, it may offer a higher limit and a lower rate than many credit cards.

So if you are buying groceries or booking a flight, a credit card usually makes more sense. If you need flexible access to funds for a larger, ongoing, or unpredictable expense, a line of credit may be the better tool.

Line of Credit vs. Personal Loan

A personal loan gives you a lump sum with fixed monthly payments and, in many cases, a fixed interest rate. It works well when you know exactly how much money you need and prefer predictable repayment.

A line of credit works better when the amount is uncertain or the expense happens in stages. You borrow only what you need instead of taking the full amount on day one. The downside is that variable rates and revolving access can make budgeting harder if you are not disciplined.

If your project has a clear price tag, a personal loan may be simpler. If the cost will unfold over time, a line of credit may offer more flexibility. The best option depends less on the lender’s ad copy and more on your spending habits, timeline, and tolerance for variable payments.

How a Line of Credit Affects Your Credit Score

A line of credit can help or hurt your credit depending on how you manage it. On-time payments can support a positive credit history. High balances, missed payments, or excessive utilization can do the opposite.

Because many personal lines of credit are reported as revolving credit, they may affect your credit utilization ratio, which measures how much revolving credit you are using compared with your total available credit. Lower utilization is generally better. If you max out your line of credit, lenders and scoring models may see that as a sign of stress.

Opening a new credit line can also trigger a hard inquiry, which may temporarily affect your score. That is usually a small issue compared with what happens next. The long-term impact depends on whether you pay on time, keep balances reasonable, and avoid treating the line like an endless extension of your paycheck.

When a Line of Credit Makes Sense

- Ongoing home projects with uncertain final costs

- Emergency expenses you may need to cover in stages

- Medical or dental bills that arrive over time

- Irregular income situations, such as freelancing or seasonal work

- Business cash flow gaps and short-term operating expenses

- Debt consolidation in specific cases where the rate and repayment plan are truly better

When a Line of Credit Can Be a Bad Idea

- You need a one-time lump sum with a clear payoff timeline

- You already struggle with revolving debt

- You are relying on borrowed money for everyday spending month after month

- You have not reviewed the fees, variable APR, or repayment rules

- You are considering a HELOC for discretionary spending that puts your home at risk

What to Check Before You Apply

Review the full cost

Do not stop at the interest rate. Check the APR, annual fees, maintenance charges, late fees, draw fees, and whether there is a penalty or special rule if the draw period ends.

Understand the repayment structure

Ask whether your monthly payment is interest-only, a percentage of the balance, or principal plus interest. Also ask what happens when the draw period ends.

Know whether the rate is fixed or variable

Variable-rate credit can be useful, but it is less predictable. You should know how rate changes could affect your monthly payment and total borrowing cost.

Check whether collateral is involved

If the line is secured, understand exactly what asset backs the credit. A lower rate is nice. Losing a house is not.

Real-World Experiences With How a Line of Credit Works

In real life, people usually do not open a line of credit because they woke up feeling glamorous. They open one because life got expensive, weird, or both. A homeowner might start a kitchen renovation thinking it will cost one amount, only to discover that cabinets, plumbing, and surprise wall issues all have their own opinions. In that situation, a line of credit can feel more practical than a lump-sum loan because the money is used in stages. You draw what you need, pay contractors as bills arrive, and avoid paying interest on money you have not touched yet.

Another common experience is the freelancer or self-employed worker with uneven income. One month is great, the next month looks like tumbleweeds and coffee. A line of credit can act as a short-term buffer for cash flow gaps. The useful part is flexibility. The dangerous part is using it so often that temporary support quietly becomes permanent dependence. That is when borrowers realize the line of credit is no longer a backup tool. It has become the budget.

People also use personal lines of credit for medical or dental expenses, especially when costs come in waves instead of one giant bill. That can be emotionally helpful because the borrower is not forced to guess the full amount in advance. But the experience is only positive when there is a repayment strategy. Without one, the balance hangs around and collects interest like an unwanted houseguest who keeps eating your groceries.

For small business owners, the experience is often tied to timing. A business may need inventory now, payroll next week, and payment from customers two weeks later. A business line of credit can smooth that mismatch. Owners often describe it as breathing room. Still, breathing room is not the same thing as profitability. If the business is borrowing repeatedly to cover chronic losses instead of short-term timing gaps, the line of credit can mask a deeper problem rather than solve it.

Then there is the HELOC experience, which tends to feel powerful at first because the borrowing limit can be much higher. People like the lower rates compared with unsecured debt. But the emotional reality is different when your home secures the balance. Borrowers who use HELOCs responsibly often say the key is treating the line like a tool for value-building expenses, such as repairs or renovations, rather than everyday consumption. In other words, using your house to finance a lasting improvement is one thing. Using it to fund a lifestyle you cannot maintain is a very different movie, and it rarely has a cheerful ending.

The best borrower experiences usually have three things in common: they knew the fees, they understood the repayment phase, and they borrowed with a clear exit plan. The worst experiences usually begin with the sentence, “I figured I’d deal with that later.” Financial products love that sentence. Borrowers usually do not.

Final Thoughts

So, how does a line of credit work? It gives you access to flexible, reusable funds up to a limit, lets you borrow as needed, charges interest on what you use, and requires disciplined repayment. It can be a smart financial tool for uncertain or ongoing expenses, especially when compared with taking a full lump-sum loan you may not need right away.

But flexibility is not the same thing as cheap, safe, or effortless. A line of credit works best when you understand the draw period, repayment terms, interest structure, fees, and impact on your credit. Used wisely, it can help you manage real-life costs. Used carelessly, it can become revolving stress with better branding.

In short: borrow for a plan, not for vibes.