Table of Contents >> Show >> Hide

- What exactly is a flash crash (and what isn’t)?

- The “getting faster” part: why modern crashes can happen in a blink

- A quick history lesson: flash crashes didn’t start in the internet age

- Real-world examples: when fast turns into “what just happened?”

- Guardrails: how today’s markets try to prevent total chaos

- Why these events feel more common lately (even when the market “seems fine”)

- The wealth-of-common-sense lesson: speed is optional for investors

- What regulators and market designers still wrestle with

- Conclusion: flash crashes are fastbut you don’t have to be

- Experiences: what ultra-fast flash crashes feel like (and what people learn afterward)

Once upon a time, a “market crash” was an all-day affair. Traders yelled, phones rang, and someone’s tie inevitably got sacrificed to the stress gods.

Today, the market can do a full emotional breakdown, ugly-cry, and recovery montage before you’ve finished microwaving leftovers.

That’s the unsettlingand oddly fascinatingtheme behind “Flash Crashes Are Getting Faster”: modern markets don’t just move fast; they

overreact fast. And because the plumbing of the system is now digital, global, and algorithm-heavy, the “whoa, what just happened?”

moments are showing up more often, and in tighter time windows.

What exactly is a flash crash (and what isn’t)?

A flash crash is a rapid, steep price moveusually downfollowed by a quick rebound. The defining feature isn’t just the drop; it’s the

speed and the snap-back. In other words: panic, then amnesia.

Not every big red day is a flash crash. Sometimes markets fall because something genuinely changedeconomic data, a policy shock, a war, a credit event.

Flash crashes are different: they often look like a temporary liquidity problem that becomes a price problem… and then becomes a story you tell at dinner.

The “getting faster” part: why modern crashes can happen in a blink

Ben Carlson’s core idea is simple: human emotions haven’t changed, but the market’s reaction time has been given a turbocharger.

We’re not trading with chalkboards and handwritten tickets anymore. Information is instant, trading is instant, and the feedback loop between fear and price

has gotten dangerously efficient.

1) Markets are now interconnected by design

Stocks, futures, options, ETFs, and global currency markets are tied together through arbitrage and hedging. If something jolts one market, the

“translation” into other markets can be automated. That’s great when things are calm. During stress, it can act like a domino line… made of dominoes

that also have jetpacks.

2) Liquidity is real… until it isn’t

In normal times, order books look deep and comfortinglike a well-stocked pantry. But during shock moments, liquidity can vanish.

Market makers widen spreads, pull quotes, or reduce size. Prices then jump to find the next available buyer.

The drop can look mysterious because it isn’t always about “new bad news.” It can be about a sudden shortage of willingness to trade at the old price.

3) Algorithmic and high-speed trading compress the timeline

Automated strategies can respond to price moves, volatility, and order flow faster than any human can react. When many systems respond similarly,

the market can get into a “self-reinforcing spiral” where selling triggers more sellingnot necessarily because fundamentals changed, but because

the microstructure is amplifying the move.

4) Leverage makes everything more dramatic

Leverage is the market’s espresso shot: a little can energize, a lot can cause trembling hands and regrettable decisions.

Leveraged positions can create forced selling through margin calls, risk limits, or volatility-targeting rules. When volatility spikes,

some strategies automatically de-riskoften at the same timeadding fuel to a fast drop.

5) Your phone is now a trading desk (and that matters)

This one is sneaky. The market’s speed isn’t just about institutions. It’s about access. The friction is gone.

You don’t have to call a broker; you can hit “sell” while standing in line for iced coffee, operating purely on vibes and adrenaline.

The problem is that fast markets + fast fingers can turn a temporary shock into a permanent mistake.

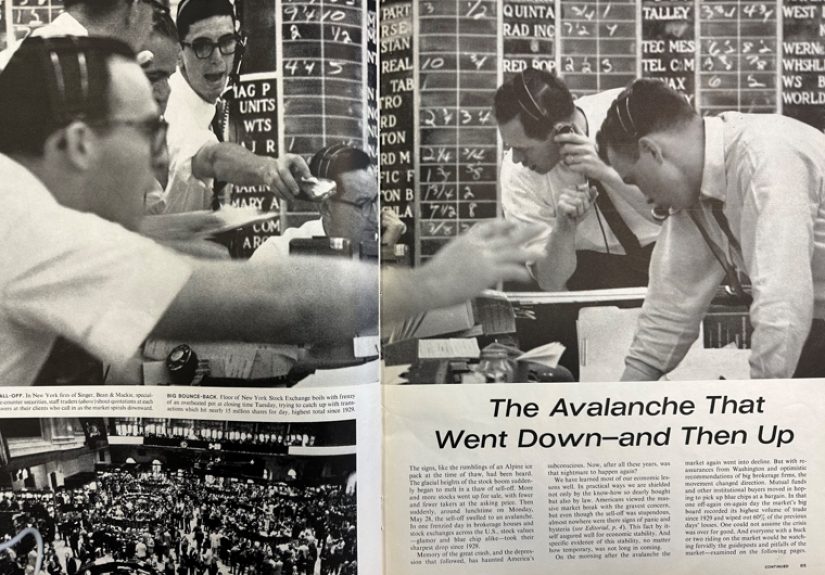

A quick history lesson: flash crashes didn’t start in the internet age

One of the most useful “wealth of common sense” reminders is that markets have always been moody.

Carlson even points to a famous example from the spring of 1962, when the market experienced a sharp one-day selloffan old-school “flash crash”

measured in hours, not milliseconds.

The difference today isn’t that fear exists. It’s that fear now has high-speed delivery.

Real-world examples: when fast turns into “what just happened?”

The May 6, 2010 Flash Crash: a modern classic

The 2010 Flash Crash is the event most people think of when they hear the term. U.S. equity markets fell sharply and then rebounded within minutes.

Investigations described how stresses in futures and equities interactedliquidity thinned, trading became disorderly, and prices detached from

what looked reasonable just moments earlier.

The big takeaway isn’t “one weird trade broke the market.” It’s that a complex, fragmented system can react unpredictably when many participants

try to manage risk at the same time.

August 24, 2015: ETFs and the opening-bell chaos

Another case study came during the August 24, 2015 volatility event, when many securitiesespecially exchange-traded productsexperienced

trading pauses and sharp, temporary dislocations. What made it messy was the combination of market opens, delayed price discovery in underlying

holdings, and volatility controls triggering across many tickers at once.

October 15, 2014: even Treasuries can get jumpy

If you think “flash crash” is only a stock thing, the U.S. Treasury market would like a word.

On October 15, 2014, Treasuries experienced a sudden burst of volatility and unusually large intraday price movements accompanied by very high volumes.

The episode became a reminder that even the world’s benchmark “safe” market can have sudden air pockets when flows collide with thin liquidity.

August 1, 2012: the Knight Capital cautionary tale

Not every “flash” event is driven by crowd panic. Sometimes it’s a technology failure that turns into a market event.

Knight Capital experienced a severe problem in an automated routing system that quickly generated massive unintended trading activity.

The moral: automation can scale good decisions… and also scale bad ones into catastrophes at record speed.

Manipulation and spoofing: when “fake liquidity” becomes a real problem

Regulators have also highlighted how manipulative practiceslike spoofingcan worsen fragile market conditions.

Spoofing attempts to create an illusion of supply or demand, which can distort order books and intensify instability during already-stressed periods.

Guardrails: how today’s markets try to prevent total chaos

After major dislocations, regulators and exchanges didn’t just shrug and say “welp.” They installed speed bumps.

Two big ones matter for investors:

1) Market-wide circuit breakers

Market-wide circuit breakers are cross-market trading halts triggered by steep declines in the S&P 500. The goal is simple: force a pause so prices

can reset and participants can regain coordination instead of stampeding all at once.

2) Limit Up–Limit Down (LULD)

LULD aims to prevent trades in individual securities from occurring too far outside a price band. If a stock moves too rapidly beyond its bands,

it can enter a limit state and potentially trigger a trading pause. This is designed to reduce “absurd prints” and curb the most extreme,

blink-and-you-miss-it price errors.

Important: these mechanisms help, but they don’t eliminate volatility. They manage the most chaotic forms of itlike putting guardrails on a mountain road.

You can still have a scary drive; you’re just less likely to launch into the canyon.

Why these events feel more common lately (even when the market “seems fine”)

One of the eeriest things about modern mini-flash crashes is that they can happen without a full-blown recession headline.

Carlson points to how a sharp, sudden swoon can occur and then reversealmost like the market briefly remembered it had anxiety, spiraled,

and then tried to act normal again.

The ingredients for these faster episodes are increasingly common:

- Global, synchronized trading where shocks travel quickly across regions and asset classes.

- Systematic strategies that adjust exposure based on volatility, momentum, or risk limitsoften simultaneously.

- Heavier use of leverage in pockets of the system, which can trigger forced selling when conditions change.

- Instant information processing where markets react to data, headlines, and narratives in real time.

- Lower friction for retail trading which can amplify emotional participation at precisely the wrong moment.

The wealth-of-common-sense lesson: speed is optional for investors

Here’s the paradox: markets are faster, but your decision-making doesn’t have to be.

In fact, if you’re a long-term investor, the best response to a fast market is often to

slow down.

The market’s job is to generate prices. It will do that with or without your emotional approval.

Your job is to avoid turning temporary volatility into permanent damage. And that usually comes down to behavior, not brilliance.

Practical ways to avoid getting steamrolled by a 10-minute panic

- Know what you own and why you own it. If your plan is “it went up last week,” a flash crash will introduce you to fear in HD.

-

Understand order types. In chaotic moments, market orders can fill at unpleasant prices. Many investors prefer to be thoughtful about

how they enter or exit positions during volatile windows. - Respect leverage. Leverage reduces your margin for error precisely when the market reduces its patience.

- Build a decision rule before the stress hits. It’s easier to be wise on a calm Tuesday than on a panicked Monday morning.

- Remember that volatility is a feature, not a bug. Markets are not designed to make you feel comfortable. They are designed to discover prices.

None of this is a promise that “everything will be fine.” It’s a reminder that the most costly mistakes often happen during the fastest moves:

selling at the bottom of a whip-saw, chasing back in at the top, and then calling it “a strategy.”

What regulators and market designers still wrestle with

Modern market structure is a tradeoff. Speed and automation can improve efficiency and reduce costs, but they also create new failure modes:

feedback loops, sudden liquidity gaps, and technology-driven accidents.

That’s why you see ongoing work on things like:

- Better risk controls for automated trading systems (so one bad line of code doesn’t become a market event).

- Volatility mechanisms (like LULD) to reduce extreme dislocations in individual names.

- Cross-market coordination so futures, equities, and ETFs don’t pull each other into disorderly spirals.

- Surveillance and enforcement to deter spoofing and other manipulative practices that can worsen fragile conditions.

Translation: the market is a high-performance machine. It needs both horsepower and brakes. We’re still improving the brakes.

Conclusion: flash crashes are fastbut you don’t have to be

Flash crashes didn’t arrive with smartphones, but smartphones sure made them easier to experience in real time (with push notifications and heart palpitations).

The modern market’s speed is the product of interconnected trading, rapid information flow, algorithmic reactions, andsometimestoo much leverage

sloshing through the system.

The biggest “common sense” point is also the simplest: the market can move fast without you moving fast.

You can design a plan that assumes volatility shows up uninvited. You can avoid letting a short-term freakout rewrite long-term goals.

And you can treat a flash crash the way you’d treat a summer storm: take it seriously, don’t stand under the tallest tree, and remember it usually passes.

Experiences: what ultra-fast flash crashes feel like (and what people learn afterward)

I don’t have personal trading experiences, but there’s a surprisingly consistent set of “this is what it felt like” stories that investors and advisors

describe after sudden, fast market breaks. They read like different genrescomedy, horror, and occasionally a coming-of-age story where the hero learns

not to hit “sell” while emotionally compromised.

Experience #1: The lunch-break whiplash. Someone checks the market around 11:55 a.m. and everything looks normal.

They go to grab food, come back, glance at a notification, and see a dramatic headline: “Stocks Slide,” “Volatility Spikes,” “Market in Turmoil.”

Their portfolio appears to be down sharply. The emotional brain does the math in record time:

“If it’s down this much in an hour, what happens by the close?” They hover over the sell button like it’s a fire alarm.

Fifteen minutes later, the market rebounds and the same person feels two conflicting emotions: relief…and annoyance that they nearly panic-sold.

The lesson most people report: the market’s speed can turn ordinary humans into day traders by accident.

Experience #2: The order-type surprise. During a fast drop, bid-ask spreads can widen and liquidity can thin.

Some investors describe placing a market order and getting a fill that felt “impossibly bad,” especially in thinly traded names or during chaotic opens.

Afterward, they learn the difference between a calm market and a stressed one: in calm conditions, execution is routine; in stressed conditions,

execution is a negotiation with a suddenly empty room. Many people come away with a new respect for patienceand for understanding how their broker handles

volatility, halts, and price bands.

Experience #3: The advisor’s phone lights up. Advisors often describe flash-crash days as “short, loud storms.”

Clients call in waves: first the worried questions (“What’s happening?”), then the urgent demands (“Should we sell?”), then the post-rebound confusion

(“Wait…so nothing happened?”). The experienced advisors don’t pretend volatility is fun. They do something more useful:

they return clients to the plan, remind them what the portfolio was built to handle, and encourage decisions made at human speed.

One of the most common takeaways from these stories is that the best portfolios aren’t just diversified across assets

they’re diversified across emotions, with processes designed to keep panic from driving the car.

Experience #4: The post-mortem clarity. After a mini flash crash, people replay the moment like a slow-motion sports highlight:

“What if I had sold?” “What if I had bought?” “Why did it happen so fast?”

Over time, many land on a calmer truth: these events are often about plumbingliquidity, leverage, automation, and crowd behavior.

The market didn’t ask permission to move. It simply did.

The investors who feel best afterward aren’t the ones who made a perfect call in the moment; they’re the ones who avoided making an irreversible mistake

during a reversible move.

If flash crashes are getting faster, the smartest adaptation may be beautifully boring:

keep your rules clear, your risk appropriate, and your finger off the “panic” button.

Let the market sprint. You can walk.