Table of Contents >> Show >> Hide

- What Bond Yields Actually Are (And Why They Won’t Stop Ruining Your Vibes)

- The Three Ingredients Inside a Treasury Yield

- So What’s a “Bond Bubble,” Anyway?

- The “Anti-Risk Bubble” Idea: When Yields Crowd Out Risk

- Yield Curve: The Market’s Mood Ring (Not a Crystal Ball)

- Duration: The Hidden Lever Attached to Your “Safe” Bond

- Supply, Auctions, and the Not-So-Secret Life of Treasuries

- Is “High Yield” a Signal of Valueor a Warning Label?

- How to Use Bond Yields Without Getting Tricked by Them

- So… Are Bond Yields the Anti-Risk Bubble?

- Investor Experiences: What “The Anti-Risk Bubble” Feels Like in the Real World

- Experience #1: “I bought bonds for safety… and watched them drop.”

- Experience #2: The T-bill honeymoon (and the reinvestment hangover)

- Experience #3: “High yields made me question every risky bet I owned.”

- Experience #4: The yield-curve fortune teller (and why it’s usually wrong on timing)

- Experience #5: “I stopped chasing and started building.”

Bond yields have a funny way of acting like the adult in the room. Stocks can throw a party, crypto can start a conga line, and real estate can casually rename itself “can’t-lose,” but bond yields? Bond yields show up with a clipboard and ask, “Cool story. What’s the cash flow, and what’s the discount rate?”

That’s why yields can feel like an anti-risk bubble: when they rise (or just stay annoyingly high), they don’t inflate fantasiesthey deflate them. Higher yields raise the bar for every risky asset on the planet. Suddenly, “maybe” projects become “nope,” leverage gets expensive, and investors rediscover the forgotten art of being picky.

So are bond yields the opposite of a bubblean expanding gravitational field that pulls risk back down to earth? Let’s unpack the mechanics, the myths, and the practical moves that keep your portfolio from turning into a cautionary tale told by a financial podcast host with dramatic background music.

What Bond Yields Actually Are (And Why They Won’t Stop Ruining Your Vibes)

A bond yield is basically the market’s “price tag” for lending money. When you buy a bond, you’re trading cash today for a stream of payments (coupon interest) plus principal at maturity. The yield translates that deal into an annualized rate so you can compare it to other optionslike CDs, cash, or taking your chances with the stock market’s mood swings.

The rule that explains 80% of bond drama

Bond prices and yields move in opposite directions. When new bonds are issued with higher rates, older bonds with lower coupons become less attractive, so their prices fall until their yields “catch up.” When rates fall, existing higher-coupon bonds look better, and prices rise.

This is why people say bonds are “safe” and then act personally betrayed when their bond fund drops 8%. The issuer might be safe, but the price still movesespecially when rates move fast.

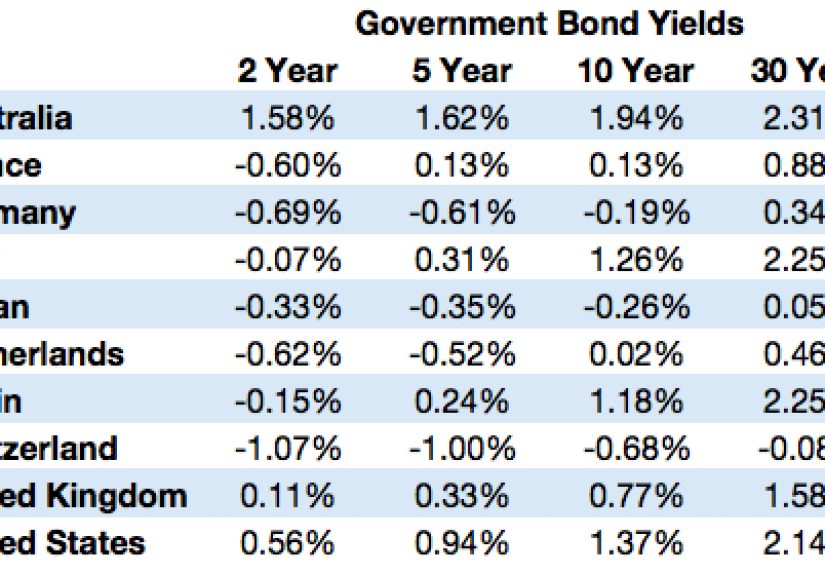

The Three Ingredients Inside a Treasury Yield

For U.S. Treasuries (the benchmark “risk-free-ish” asset in dollar markets), yields tend to reflect three big components:

1) Expected path of short-term interest rates

Markets constantly guess where the Federal Reserve’s policy rate is headed. If investors think short-term rates will stay higher for longer, longer-term yields often rise too (though not always in perfect sync).

2) Inflation expectations (nominal vs. real)

Nominal Treasury yields include compensation for expected inflation. A common way investors infer inflation expectations is by comparing nominal Treasuries to TIPS (Treasury Inflation-Protected Securities). The gap between them is often called “breakeven inflation,” and it represents the inflation rate at which an investor would be indifferent between the two (in a simplified sense).

3) The term premium (a.k.a. “pay me for the uncertainty”)

Even if everyone agreed perfectly on future short rates and inflation (they don’t), long-term bonds still carry risk: rates can change, inflation can surprise, and investors can demand extra compensation for holding longer maturities. That extra compensation is often discussed as the term premium.

Put together, a simplified mental model looks like this:

Nominal yield ≈ real yield + expected inflation + term premium

So What’s a “Bond Bubble,” Anyway?

People usually shout “bond bubble!” when they think bond prices are too high (and yields too low) relative to fundamentals. The classic argument goes like this:

- Central banks buy lots of bonds (directly or indirectly), pushing prices up and yields down.

- Investors “reach for yield,” accepting lower returns and more risk just to earn something.

- Eventually, inflation or growth returns, rates rise, and bond prices fallpop goes the bubble.

A key point: unlike dot-com stocks or meme coins, bonds have a maturity date and a cash-flow schedule. That makes them harder to “bubble” in the pure fantasy sense. But prices can still get stretched if the market is paying too much for safety, liquidity, or central-bank backstopsespecially when yields hover near historic lows.

What the “pop” looked like in real life

When inflation surged and policy rates rose quickly in the early 2020s, bond prices fell hard. That wasn’t a failure of math; it was the math doing its job at high speed. Long-duration bonds got hit the most, and broad bond indexes saw historically painful declines.

The “Anti-Risk Bubble” Idea: When Yields Crowd Out Risk

Here’s the intuition behind calling bond yields an “anti-risk bubble”: when yields are sufficiently attractive, safe returns become competitive. That changes behavior across markets:

- Discount rates rise: higher yields increase the discount rate used to value future cash flows, which tends to pressure long-duration equities (think growth stocks), private valuations, and speculative narratives.

- Cash stops being trash: when short-term yields are meaningful, investors don’t feel forced into risk just to keep up with inflation or meet return targets.

- Leverage gets expensive: borrowing costs rise, which can cool real estate, private credit, and levered strategies.

- “Good enough” becomes a strategy: a portfolio can hit goals with less drama when high-quality bonds offer real income.

In that sense, rising yields can behave like a reverse bubble: instead of inflating asset prices through cheap capital, they tighten the filter on what deserves funding.

Why this feels like a bubble anyway

The word “bubble” sneaks back in because investor behavior still swings between extremes: “Bonds are useless” (when yields are low) and “Why own anything else?” (when yields are high). If everyone piles into the same “safe yield” trade without respecting interest-rate risk, you can still get crowded positioning just with a different emotional soundtrack.

Yield Curve: The Market’s Mood Ring (Not a Crystal Ball)

The yield curve plots yields across maturitiesshort-term bills, intermediate notes, long-term bonds. In normal times, longer maturities yield more than shorter ones (because investors demand compensation for time and uncertainty).

But sometimes the curve invertsshort-term yields exceed long-term yields. Historically, certain inversions (like the spread between 10-year and 3-month Treasuries) have had a reputation for preceding recessions.

Here’s the part people miss: the yield curve is not “predicting” recessions out of spite. It’s reflecting a market story: short rates are high now, but investors expect growth and inflation to cool enough that future rates will be lower. That story can be right for the wrong reasons, wrong for the right reasons, or complicated because reality loves plot twists.

Duration: The Hidden Lever Attached to Your “Safe” Bond

If you remember one risk concept, make it duration. Duration is a measure of how sensitive a bond’s price is to changes in interest rates. A rough rule of thumb often taught to investors is:

A bond (or bond fund) with a duration of 7 may move about 7% in price for a 1% (100 bps) move in rates, in the opposite direction.

This isn’t magic; it’s just geometry applied to discounted cash flows. Longer maturity and lower coupon generally mean higher duration, which means more sensitivity. That’s why “locking in” a higher yield with a long bond can still hurt if yields rise further.

The practical takeaway

Don’t buy long-duration bonds just because the yield looks tasty. Buy them because they match your time horizon and your role-in-portfolio. If you need the money in two to five years, a 30-year bond is not “conservative”it’s a roller coaster with a cardigan on.

Supply, Auctions, and the Not-So-Secret Life of Treasuries

Treasury yields aren’t driven only by inflation and the Fed. They also reflect supply and demand dynamics: how much debt the U.S. Treasury issues, how investors absorb it, and how global savings flows move.

Treasury issuance happens through regular auctions across bills, notes, and bonds. The cadence is predictable, and the market watches auction demand as a real-time sentiment check: strong demand can support prices (lower yields), while weak demand can nudge yields higher as the market demands more compensation.

Translation: yes, macro matters. But sometimes the week’s “bond story” is as simple as: “A lot of bonds showed up to the party, and buyers weren’t in a hugging mood.”

Is “High Yield” a Signal of Valueor a Warning Label?

A higher yield can mean “better expected return,” but it can also mean “higher risk,” depending on the type of bond:

- Treasuries: higher yields mostly reflect inflation expectations, real-rate changes, and term premium shifts.

- Investment-grade corporates: yields reflect Treasury rates plus credit spreads (default and downgrade risk).

- High-yield (“junk”) bonds: yields can be high because recession risk and default risk are real, not theoretical.

This is where the “anti-risk bubble” framing is useful: higher Treasury yields can pull money away from risky credit. If an investor can earn an attractive yield in Treasuries, they may demand a much larger spread to take corporate risk. That can tighten financial conditions and cool the broader risk appetite.

How to Use Bond Yields Without Getting Tricked by Them

Think of bond yields as a tool, not a prophecy. Here are strategies investors use to benefit from higher yields while respecting the risks:

1) Match maturity to your timeline

If the money has a date attachedtuition, a home down payment, a business expensebuild a ladder of Treasuries, CDs, or high-quality bonds that mature near when you’ll need cash. This reduces the urge to panic-sell at a bad time.

2) Diversify across duration instead of making one big bet

A barbell approach (some short-term, some intermediate/long-term) can help balance reinvestment risk and price sensitivity. You’re not trying to win the “best yield” contest; you’re trying to make your future self say, “Wow, past me was surprisingly reasonable.”

3) Consider inflation protection thoughtfully

TIPS can help when inflation surprises to the upside, but they behave differently from nominal bonds because their yields are “real.” Investors often use a mixsome nominal Treasuries for general stability, some TIPS as an inflation hedge.

4) Don’t confuse yield with return

The yield you see today is not the same thing as the return you’ll get tomorrowespecially in bond funds where holdings roll and prices fluctuate. Yield is an input; realized return depends on rates, defaults (for credit), fund structure, and your holding period.

5) Treat “calling the top in yields” like calling the top in anything

Could you time it perfectly? Sureright after you win a coin-flip tournament against a room full of statisticians. A more durable approach is to scale in: build exposure in steps, keep maturities aligned with goals, and accept that nobody gets to buy the exact bottom tick with clean hands.

So… Are Bond Yields the Anti-Risk Bubble?

They can bedepending on what you mean by “bubble.”

If you mean “a force that expands and reshapes markets,” then yes: higher yields can act like a powerful counterweight to risk-taking. They offer a competing source of return, raise discount rates, and make leverage less casual. That’s anti-bubble behavior.

But if you mean “a crowding phenomenon where people overdo it,” then also yes: investors can crowd into the same “safe yield” trade, underestimate duration risk, or assume today’s yields are permanently generous. Bonds don’t eliminate risk; they rearrange it.

The healthiest frame is simple: bond yields are the economy’s price of time and uncertainty. When that price rises, risk assets have to earn their keep. When it falls, optimism gets cheaper. Either way, the yield market is less like a bubbleand more like gravity.

Investor Experiences: What “The Anti-Risk Bubble” Feels Like in the Real World

Below are common experiences investors report when bond yields start acting like an anti-risk bubblepulling attention, capital, and emotion away from riskier corners of the market. These aren’t fairy tales; they’re patterns that show up repeatedly whenever rates shift quickly and portfolios have to renegotiate what “safe” really means.

Experience #1: “I bought bonds for safety… and watched them drop.”

Many investors learned the hard way that “safe issuer” doesn’t mean “stable price.” Someone buys a long-term Treasury fund because Treasuries are backed by the U.S. governmentfair! Then yields rise, the fund falls, and suddenly the investor is Googling “duration” like it’s a medical symptom. The emotional whiplash is predictable: “Bonds are supposed to be boring!” True. But boring doesn’t mean motionless.

The lesson investors often take away is practical: if you need price stability, keep maturities shorter. If you’re buying longer maturities, do it for a reasonusually to match long-term liabilities or to balance equity risk and accept that short-term mark-to-market swings are part of the deal.

Experience #2: The T-bill honeymoon (and the reinvestment hangover)

When short-term yields rise, people fall in love with T-bills. The appeal is obvious: you can earn meaningful income without committing for long. Investors often describe it as “finally getting paid to wait.” Portfolios get calmer. Risk appetite cools. And thensometimesyields start to drift lower, and reinvestment becomes the new stress.

That’s reinvestment risk: the risk that you’ll have to roll your money into lower yields later. Investors who lived through ultra-low-rate eras remember this vividly. The fix isn’t to panic-buy a 30-year bond out of spite; it’s to ladder maturities. A ladder spreads reinvestment over time. You’ll roll some bonds in a high-yield environment and some in a lower-yield environment, which is basically dollar-cost averaging for fixed income.

Experience #3: “High yields made me question every risky bet I owned.”

This is the anti-risk bubble in action. When Treasuries and high-quality bonds offer attractive yields, investors start doing something radical: they compare. A speculative stock with no earnings is no longer competing with “cash at basically zero.” It’s competing with a bond yield that can cover a chunk of a retirement plan without requiring an emotional support group.

Investors often report trimming the noisiest parts of their portfolios in these periodsoverlevered real estate exposure, lower-quality credit, or expensive growth equitiesbecause the opportunity cost of risk rises. The portfolio feels “cleaner,” not because bonds are exciting, but because the return target can be met with fewer heroic assumptions.

Experience #4: The yield-curve fortune teller (and why it’s usually wrong on timing)

People love to use the yield curve like a weather app: “Inversion detectedrecession in 6 to 12 months!” Then 6 to 12 months pass and the economy does something inconveniently complicated. The yield curve can be informative, but investors frequently discover that it’s a signal, not a schedule.

A common “grown-up” takeaway is to use curve signals to stress-test the portfolio instead of trying to time a single outcome. What happens if growth slows? What happens if inflation re-accelerates? What happens if yields fall quickly and you’re stuck reinvesting at lower rates? Investors who plan for multiple scenarios tend to feel less compelled to make all-or-nothing moves based on one line chart.

Experience #5: “I stopped chasing and started building.”

This is the best outcome of higher yields: investors shift from performance-chasing to structure-building. They build ladders. They match maturities to goals. They hold a mix of nominal bonds and inflation protection. They accept that the bond portion of the portfolio is not there to be coolit’s there to be dependable.

If you’re looking for a one-sentence summary of these experiences, it’s this: When yields are high, the market offers you a chance to get paid for being patientif you respect the risks that come with that paycheck.