Table of Contents >> Show >> Hide

- What Counts as a Bear Market (and Why People Argue About It)

- Losses vs. Time: The Two Ways Bear Markets Hurt

- The Longest Bear Markets (Why They Drag On)

- The Shortest Bear Markets (Why They Snap Back)

- So… How Long Do Bear Markets Usually Last?

- Bear Markets vs. Recessions: Related, Not Identical Twins

- What a “Wealth of Common Sense” Bear-Market Playbook Looks Like

- Putting the “Longest vs. Shortest” Lens to Work

- Extra Perspective: of “Been There” Experiences (Without Pretending We’re Psychic)

- Conclusion

Bear markets have a special talent: they make smart adults forget how math works and start treating their retirement accounts like a haunted house.

One day you’re calmly “long-term investing,” and the next you’re Googling, “How long do bear markets last and can I hibernate until it’s over?”

This is where a little wealth of common sense goes a long way. Yes, bear markets can be brutal. No, they’re not new. And surprisingly often,

they’re shorter than they feel (time stretches when your portfolio is screaming).

In this guide, we’ll break down what counts as a bear market, highlight the longest and shortest downturns in modern U.S. stock history,

andmost importantlypull practical lessons you can actually use when the headlines are acting like the sky is falling.

What Counts as a Bear Market (and Why People Argue About It)

The most common definition is simple: a bear market is a decline of 20% or more from a market peak to a subsequent low.

Some analysts use intraday prices; others use closing prices. Some track the S&P 500; others look at the Dow or Nasdaq.

And yes, people can (and do) turn this into a spreadsheet hobby.

A practical, commonly used approach is to define bear markets using closing levels and measure duration from the prior peak close

to the lowest close after the index is down 20% (including weekends and holidays). In other words, it’s not just “the vibe,” it’s the data.

Correction vs. Bear Market

A correction is typically a drop of about 10%–19.9% from a recent high. A bear market starts at 20%.

That 0.1% difference is the line between “healthy pullback” and “everyone suddenly becomes a macroeconomist.”

Losses vs. Time: The Two Ways Bear Markets Hurt

Bear markets deliver pain in two flavors:

- Depth (loss): How far the market falls from peak to trough.

- Duration (time): How long it takes to reach the bottomand how long it takes to get back to the previous high.

The second one is sneakier. A fast crash is terrifying, but a long, grinding decline can be psychologically exhausting. It’s the difference between

ripping off a Band-Aid and living with a papercut that keeps finding lemon juice.

Looking at post–World War II U.S. bear markets, one common-sense takeaway is that the “typical” bear market has historically been measured in

months, not decadesand the “roundtrip” back to breakeven has often been under a few years. But “average” is a dangerous word:

averages hide the fact that some bears are quick, and some have the stamina of a marathon runner.

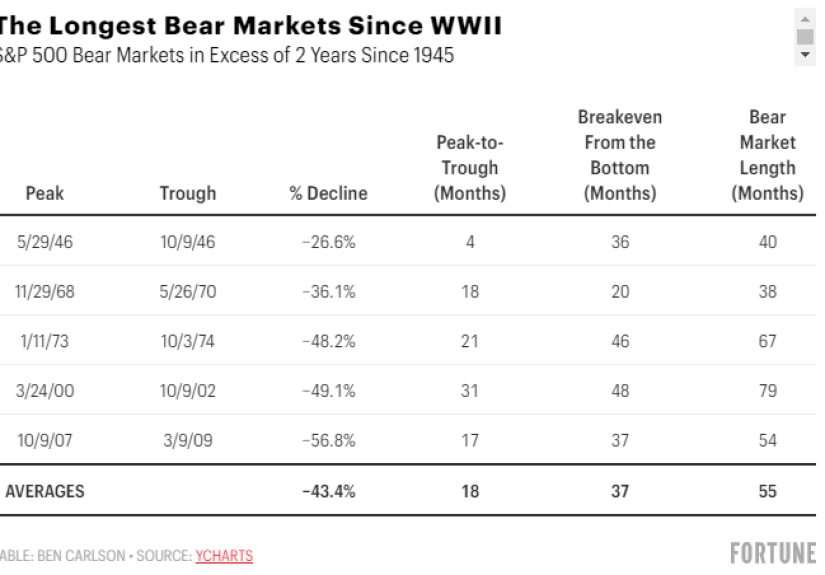

The Longest Bear Markets (Why They Drag On)

Long bear markets usually come from bigger structural or cyclical problems: bubbles deflating, financial systems cracking, inflation shocks,

or recessions that aren’t just a speed bump. They tend to involve more than one “bad thing” at the same timebecause markets are overachievers

when it comes to drama.

Notable long bear markets (S&P 500, peak-to-trough)

| Bear market | Rough story | Peak-to-trough duration | Approx. decline |

|---|---|---|---|

| 2000–2002 | Dot-com bubble deflates (plus multiple shocks) | ~929 days | ~-49% |

| 2007–2009 | Global Financial Crisis (credit & housing unwind) | ~517 days | ~-57% |

| 1973–1974 | Stagflation era stress (inflation + growth concerns) | ~630 days | Deep multi-year drop |

Notice what these have in common: they weren’t “one weird day.” They were multi-act tragedies. The dot-com crash wasn’t just about tech stocks

it was an unwinding of expectations. The financial crisis wasn’t just “stocks down,” it was a system-wide stress test.

And in the 1970s, inflation and growth worries rewired how investors thought about value, rates, and risk.

Common-sense lesson from the long bears

If the underlying problem is structural (a bubble, a banking crisis, stubborn inflation), recoveries can take time.

That doesn’t mean “never invest again.” It means your plan should assume that markets can be underwater long enough to tempt you into the

worst possible decision: selling because you’re tired.

The Shortest Bear Markets (Why They Snap Back)

Short bear markets tend to be event-driven: a sharp shock hits, prices fall fast, and then policy responses and improving expectations

help the market rebound. These are still scary in real timebecause your brain doesn’t care that it’s “only” been three weeks.

The poster child: 2020

In early 2020, U.S. stocks fell into bear market territory at record speed, and the S&P 500’s peak-to-trough bear market lasted about

one month. The drop was swift, and the recovery was unusually fast compared with many historical episodes.

The key point isn’t “2020 will happen again the same way.” It’s that the market can deliver a full-blown bear market

faster than most people can finish reorganizing their watchlist.

Common-sense lesson from the short bears

When downturns are fast, the rebound can be fast toowhich is exactly why panic-selling is so destructive.

If you sell after a sudden drop, you’re essentially volunteering to miss the part where markets do what they do best: recover.

So… How Long Do Bear Markets Usually Last?

The honest answer is: it depends. But “it depends” is not satisfying when you’re staring at a red screen.

So here are the helpful patterns investors lean on:

-

Bear markets are common and historically shorter than bull markets.

Over long periods, data summaries often show bears averaging under a year, while bull markets typically last longer. -

There’s a wide range.

Some bears bottom in a few months (or weeks). Others can grind for years. -

Recovery time matters.

The time back to the previous peak can be longer than the time to the bottomespecially after big, systemic shocks.

One particularly useful framing is the “roundtrip”: peak → trough → back to prior peak. Historically, that roundtrip has often been measured

in a handful of years, not a lifetimeyet the experience can feel like it’s lasting longer than your group chat’s most dramatic breakup.

Bear Markets vs. Recessions: Related, Not Identical Twins

Many bear markets happen around recessionsbut they aren’t the same thing.

Recessions are dated by economic activity (jobs, output, income, etc.). Bear markets are dated by market prices.

Sometimes stocks fall hard without a recession arriving on schedule. Sometimes the economy weakens and markets bottom before the data looks “better.”

For example, the official U.S. recession around the COVID shock had a peak in early 2020 and a trough in spring 2020extremely short by historical

recession standards. Meanwhile, markets can front-run recoveries or overreact to fears that don’t become reality.

Common-sense takeaway

If you wait for “certainty” (the economy is fine, inflation is fixed, the news is calm), you often get it at a higher price.

Markets don’t ring a bell at the bottom. They barely send a push notification.

What a “Wealth of Common Sense” Bear-Market Playbook Looks Like

Here’s the practical partbecause history is only useful if it changes what you do next.

1) Define your time horizon before the panic

If you need the money soon (near retirement, big purchase, short runway), your risk plan should reflect that.

If you’re decades from retirement, downturns are unpleasantbut they’re also the periods where long-term investors accumulate shares at lower prices.

2) Separate “watching markets” from “managing money”

Watching markets is entertainment. Managing money is a process. In bear markets, the entertainment gets addictive and unhelpful.

If your plan is sound, you don’t need to stare at every tick like it’s a heart monitor.

3) Use rules: rebalance, don’t react

Rebalancing is the boring superpower: it nudges you to buy what’s down and trim what’s up, without needing to predict the future.

In a bear market, rebalancing can feel emotionally backwardwhich is precisely why it works.

4) Don’t confuse speed with permanence

Fast drops feel like “this time is different.” Sometimes the catalyst is genuinely new. But markets have a long track record of eventually moving

onoften sooner than the average investor expects when they’re in the middle of it.

5) Protect the plan from the headline cycle

A bear market will always come with a story that sounds uniquely terrifying: inflation, rates, wars, tech bubbles, credit crises, pandemics,

trade shockspick your monster. The story matters, but it can also hypnotize you into abandoning a long-term strategy at the worst time.

Putting the “Longest vs. Shortest” Lens to Work

Here’s a simple way to use the longest-and-shortest framework without turning into the kind of person who says “actually” at parties:

-

If the decline is event-driven and liquidity returns quickly, history shows some bear markets can be short and sharp.

Your biggest risk is panic-selling and missing the rebound. -

If the decline reflects a structural reset (bubble unwinding, banking stress, entrenched inflation),

the bear market can last longer. Your biggest risk is “decision fatigue” that convinces you to quit near the bottom. -

In both cases, discipline beats prediction.

You don’t need to call the bottom. You need a plan you can follow while you’re scared, annoyed, or both.

Extra Perspective: of “Been There” Experiences (Without Pretending We’re Psychic)

Let’s talk about the human side, because bear markets aren’t just numbersthey’re experiences. And while everyone’s situation is different,

many investors report eerily similar emotional patterns.

Experience #1: The “I’ll just wait for things to calm down” trap.

A lot of people start a bear market with a reasonable idea: “I’ll pause contributions until volatility settles.”

The problem is that “calm” usually arrives after prices rebound. By the time the news sounds less terrifying,

the market may already be up double digits from the lows. Investors who kept automatic contributions running often describe it as

accidentally doing the right thinglike finding $20 in your winter coat, except the coat is your 401(k).

Experience #2: The slow bear is more exhausting than the fast bear.

In a fast crash, fear is the main emotion. In a long bear market, fear morphs into frustration and boredomtwo emotions that are underrated

portfolio hazards. People start asking, “Why am I investing if it never goes up?” (It’s going up; it’s just doing it rudely, later.)

The “grind” is where investors are most likely to abandon diversification, chase whatever worked last year, or decide they’re suddenly

a 100% cash person. The common-sense move is to make fewer decisions, not morestick to rebalancing rules, keep contributions consistent,

and reduce headline consumption so you don’t confuse feelings with facts.

Experience #3: The day you stop checking is often the day you start recovering.

Many investors notice a weird phenomenon: the more they check, the worse they feelregardless of what the market does.

Some people set boundaries (checking weekly instead of hourly), and it improves decision-making almost immediately.

It’s not denial; it’s recognizing that your portfolio doesn’t need play-by-play commentary. If you’re investing for years or decades,

constant monitoring is like watching bread rise in the oven. You’ll ruin it… and you’ll still be hungry.

Experience #4: The “common sense” win is usually unglamorous.

The investors who navigate bear markets best rarely do something heroic. They do something repetitive:

they keep saving, diversify, rebalance, and avoid big, emotional moves. It doesn’t feel bold. It feels boring.

But over time, boring beats brilliantespecially when “brilliant” is actually “panicked with confidence.”

Experience #5: The lesson everyone learns too latethen (hopefully) never forgets.

After a bear market ends, people look back and realize they didn’t need to predict the bottom.

They needed to avoid the major unforced errors: selling into fear, abandoning a plan, or going all-in on a new strategy because it felt safer.

The irony is that the “safest” emotional choice in the moment is often the riskiest long-term choice.

Common sense doesn’t eliminate uncertainty; it helps you behave well in the presence of uncertainty.

Conclusion

The longest bear markets tend to be tied to bigger economic and financial resetsevents that take time to unwind and rebuild confidence.

The shortest bear markets are often fast shocks that reverse when conditions stabilize and liquidity returns.

Both feel awful in real time. Both are survivable with a plan.

The wealth of common sense lesson is simple: you don’t need a perfect forecast. You need durable behaviorsdiversification,

realistic time horizons, rules-based rebalancing, and the discipline to keep investing when it doesn’t feel good.

Bear markets don’t last forever, but your decisions during them can.