Table of Contents >> Show >> Hide

- Why the Title Fits in 2026

- The Three Big Reasons Options Keep Growing

- How Options Actually Influence Stock Prices

- 0DTE: The Tiny Contracts With Outsized Attention

- Retail Traders Changed the Culture, Not Just the Volume

- Options Are Also Eating Portfolio Construction

- The Bull Case and the Bear Case

- What Investors Should Take Away

- Final Thoughts: The Market Has a New Operating System

- Extended Perspective: What This Feels Like in Real Life

- SEO Tags

The stock market used to be easier to explain at family dinner. You bought shares in a company, waited patiently, and hoped the business made more money than it spent. Very wholesome. Very Norman Rockwell. Now, however, a growing share of the action is happening in options, where traders rent exposure, borrow time, and occasionally behave as if expiration day is a personality trait.

That is the spirit behind the phrase “Options Are Eating the Stock Market.” It sounds like clickbait in a nice blazer, but the idea is serious. The U.S. stock market is no longer driven only by investors buying and selling shares. It is increasingly shaped by derivatives, especially listed options, and by the dealers, hedgers, income funds, and short-term traders who live inside that world. Stocks are still the meal, but options are starting to control the menu.

This does not mean the cash equity market is disappearing. It means the behavior of stocks, especially over short periods, is increasingly influenced by options volume, options positioning, and the hedging flows created by those trades. If you have ever wondered why a stock can levitate, freeze near a strike price, or whip around like it drank four espressos before lunch, options are often somewhere in the background, fiddling with the controls.

Why the Title Fits in 2026

The case starts with scale. Options trading is not some niche corner of the market anymore. It is enormous. Listed options volume has been breaking records, and the growth has not been limited to one weird month or one meme-stock fever dream. It has become a structural feature of modern markets.

That matters because options do more than express an opinion. They can create feedback loops. When traders buy calls, sell puts, write covered calls, chase zero-day contracts, or pile into expiration trades, someone on the other side often has to hedge. Those hedges usually involve buying or selling the underlying stock or a related index future. In other words, derivatives do not just sit on top of the stock market like decorative frosting. They can reach down and move the cake.

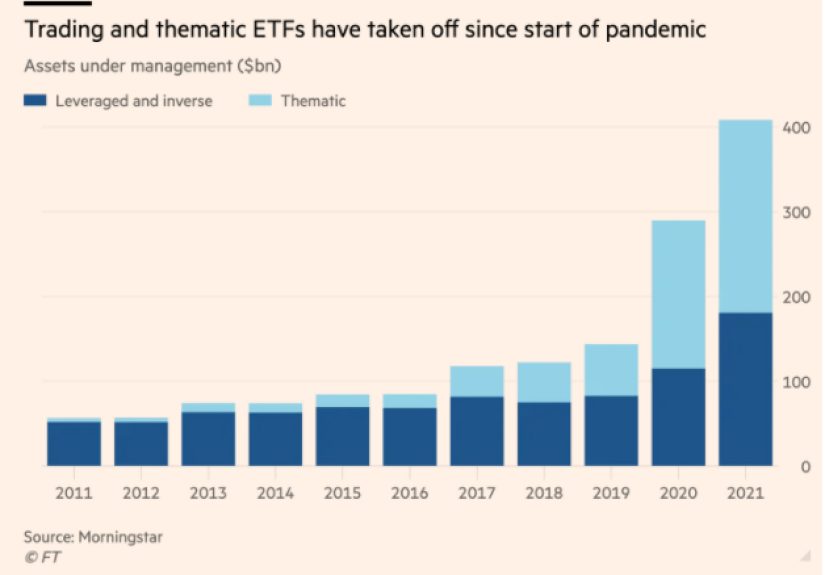

The phrase also works because options are now being used for wildly different purposes all at once. Some investors use them to hedge. Some use them to generate income. Some use them to speculate on intraday moves with the financial equivalent of a jet ski and poor impulse control. And some access them indirectly through ETFs built around covered calls, collars, or defined-outcome strategies. All of that adds up to one clear message: options are no longer a side dish.

The Three Big Reasons Options Keep Growing

1. They offer cheap, fast, dramatic exposure

Options let traders control a lot of notional exposure with relatively little capital. That is the appeal. A stock investor may need thousands of dollars to build a meaningful position. An options trader can place a much smaller bet and still get a large payoff if the move arrives on schedule. Of course, the market has a dark sense of humor, so the move often arrives right after the option expires worthless. But the appeal remains obvious.

This is especially true in the world of 0DTE options, or zero-days-to-expiration contracts. These are options traded on the day they expire. They are cheap, fast, highly liquid, and brutally unforgiving. Time decay is no longer a slow leak. It is a trapdoor.

2. There are more expiration dates than ever

Part of the explosion in options activity is simple logistics. There are now more opportunities to trade expiring contracts because exchanges have added more daily expirations to major index products. When more contracts expire more often, more traders show up to play. That does not automatically mean the market is doomed. It does mean the market is living with a much denser calendar of hedging, rolling, and expiration-related flows.

3. Options now serve both thrill-seekers and retirees

This is what makes the trend so powerful. Options are not just attracting gamblers. They are also attracting income investors. Covered-call ETFs, buffer funds, and other options-based products have brought derivatives into mainstream portfolios. The same market that offers lottery-ticket intraday bets also offers yield strategies for investors who want cash flow and some downside trade-offs. It is as if the casino started sharing a building with a retirement seminar.

How Options Actually Influence Stock Prices

This is where things get interesting. And by interesting, I mean “the stock did something weird and now everyone on television is pretending it was obvious.”

When a large amount of options activity builds up around certain strikes or expirations, market makers and dealers often hedge their exposure by trading the underlying stock or index futures. That hedging process is heavily influenced by delta and gamma, two options sensitivities that sound like villains in a superhero movie but are actually useful market tools.

Delta measures how much an option price is expected to change when the underlying stock moves. Gamma measures how fast that delta changes. As expiration gets closer, gamma can become much more sensitive. That means a small move in the stock can force a dealer to make a bigger adjustment than expected. Buy more stock here. Sell more stock there. Repeat until someone on financial social media declares they have solved market structure forever.

Sometimes those hedging flows can dampen volatility. Dealers may buy weakness and sell strength, which can pull prices back toward a strike and make the market seem oddly calm. Other times, especially during sharp moves or around crowded positions, the same machinery can amplify volatility. The result can be faster intraday swings, dramatic reversals, or a stock “pinning” near a heavily traded strike into expiration.

That is one reason the stock market can look less like a weighing machine in the short term and more like an algorithmic tug-of-war.

0DTE: The Tiny Contracts With Outsized Attention

No discussion of modern options trading is complete without 0DTE. These contracts have become the poster child for the new derivatives-heavy market. Supporters say they are efficient tools for tactical hedging around known events such as inflation reports, jobs data, and Federal Reserve meetings. Critics say they encourage ultrashort-term speculation and can make intraday price action more fragile.

Both sides have a point.

On one hand, 0DTE contracts can help institutions manage exposure very precisely. If a portfolio manager wants protection for one afternoon and not for the next three weeks, a same-day option can do the job. On the other hand, their low upfront cost and rapid payoff profile also make them attractive to retail traders chasing quick gains. That combination of professional hedging and retail speculation is part of what makes the market so noisy.

The most important thing to understand is that 0DTE does not automatically equal chaos. Their market impact depends on who owns them, who sold them, where they are struck, and how dealers hedge as prices move. In a balanced market, they may simply add activity. In a stressed market, they can become accelerants.

Retail Traders Changed the Culture, Not Just the Volume

Retail investors did not invent options, but they absolutely helped change the mood around them. During the meme-stock era, options became part investment tool, part status symbol, part internet content genre. The call-buying frenzy in names tied to online communities showed how options could magnify sentiment and feed back into stock prices.

And that culture did not vanish when the loudest meme-stock headlines cooled down. It matured. Retail traders still show up in option flows, especially in high-beta names, event-driven trades, and short-dated contracts. In bursts of speculation, call-to-put activity can climb sharply, and options volume in a handful of retail-favorite stocks can explode. Even when that enthusiasm is concentrated in a few names, it can shape headlines, volatility, and day-to-day price behavior far beyond the original trade.

The retail story also matters because it pushed options into the mainstream imagination. A generation of investors now thinks of the market not just in terms of shares bought and held, but in terms of strikes, expirations, premiums, volatility, and payoff diagrams. That is a profound cultural shift. Wall Street changed, and so did Main Street’s vocabulary.

Options Are Also Eating Portfolio Construction

It is not just trading desks and day traders. Options have started to reshape how ordinary investors build portfolios.

Consider covered-call ETFs. These funds own stocks and sell call options to generate income. The pitch is simple: trade away some upside in exchange for steady option premium. In a choppy market, that can feel appealing. In a runaway bull market, it can feel like watching your neighbor win a race while you collect participation coupons.

Then there are buffer ETFs and other defined-outcome products that use options to create preset trade-offs between upside and downside. These strategies package derivatives into something that looks and feels more like traditional investing. That makes options more accessible, but it also means more of the market’s behavior is now filtered through options mechanics, even for people who never place a single contract trade themselves.

So when we say options are eating the stock market, we do not just mean they are dominating volume. We also mean they are changing the way investors seek income, manage risk, and define success. The modern portfolio is increasingly built with options, wrapped in funds, and sold with plain-English marketing.

The Bull Case and the Bear Case

The bull case

Options can make markets more complete. They allow investors to hedge risk, express views efficiently, and manage exposures with precision that cash equities alone cannot provide. They can reduce the cost of adjusting positions, improve liquidity in popular underlyings, and offer strategies for income or protection that many investors genuinely want.

The bear case

Options can also increase fragility. They compress time horizons. They reward leverage. They can attract speculative flows that have little to do with long-term business fundamentals. And because hedging flows can spill into the underlying stock market, the derivatives tail can sometimes wag the cash-market dog.

The truth, as usual, lives between the extremes. Options are neither pure poison nor magic. They are tools. The issue is that the tools are now so large, so fast, and so embedded in market structure that ignoring them is no longer possible.

What Investors Should Take Away

If you are a long-term investor, the rise of options does not mean you need to become a full-time volatility whisperer. But it does mean you should stop assuming every short-term stock move is a clean read on fundamentals. Sometimes a stock jumps because earnings improved. Sometimes it jumps because call buying forced hedging. Sometimes it stalls because covered-call overwriting caps the enthusiasm. Sometimes it gets pinned near a strike because expiration mechanics are doing their strange little dance.

The practical takeaway is humility. A market dominated by options can look irrational in the short run even when it is functioning exactly as designed. That does not make it broken. It does make it different.

And for traders who are tempted by the speed and leverage of options, the warning label remains in giant letters. These instruments can be useful, but they are not forgiving. Short-dated options decay fast. Complex strategies are still complex no matter how clean the brokerage app looks. And selling options without understanding the risk can turn a clever idea into a very expensive life lesson.

Final Thoughts: The Market Has a New Operating System

The stock market still runs on earnings, valuations, rates, and macroeconomic expectations over the long term. But in the short term, especially intraday and around expirations, it increasingly runs on options. That is what the title gets right.

Options are eating the stock market not because stocks no longer matter, but because derivatives increasingly shape how stocks trade, how portfolios are constructed, how volatility behaves, and how investors participate. The market’s plumbing has become part of the story. Sometimes it dampens panic. Sometimes it amplifies frenzy. Often it does both in the same week, because apparently subtlety is no longer fashionable.

The old stock market was about ownership. The new stock market is still about ownership, but now it comes with overlays, hedges, expirations, dealer books, gamma effects, and income wrappers. Same market. Different operating system.

Extended Perspective: What This Feels Like in Real Life

In practical terms, living through an options-heavy market feels different from the slower, cleaner equity market many investors imagine from textbooks. Price action has a new personality. You can wake up to a calm market, watch a data release hit at 8:30 a.m., see futures lurch, and then spend the next two hours wondering whether the move is about economics, positioning, or a giant knot of expiring contracts being kicked down the road in real time. The answer is often “yes.”

One of the strangest experiences is watching stocks behave as if they are magnetized. A name with heavy open interest around a certain strike can drift back toward that level late in the day, as if some invisible hand keeps pulling it into the middle. To long-term investors, it can look absurd. To options professionals, it can look like Tuesday.

There is also a psychological difference. In a traditional stock market mindset, investors ask whether a company is cheap, growing, overhyped, or durable. In an options-driven market, people ask what the expected move is, where the dealer positioning sits, whether implied volatility is rich or cheap, and how much gamma is stacked near the current price. Those are not silly questions. But they pull attention toward shorter horizons and more tactical thinking.

That shift changes behavior. It encourages faster reactions, tighter stop levels, more event trading, and a growing obsession with the next few hours instead of the next few years. Even investors who never trade options can feel the effect. They see a stock swing wildly after a perfectly ordinary earnings report and conclude that the market has lost its mind. Sometimes the market has not lost its mind at all. It has just become extremely sensitive to the positioning wrapped around the event.

There is also something oddly democratic about this era. A giant institutional hedge, a retail call-buying spree, and an options-based ETF rebalance can all hit the same underlying market in overlapping ways. The tape reflects all of them. The result is a market that feels more crowded, more layered, and more reactive than it did a decade ago.

For disciplined investors, this environment can be frustrating, but it can also be clarifying. It reminds you that short-term price action is not always wisdom. Sometimes it is mechanics. Sometimes the market is not making a grand statement about value. Sometimes it is simply processing leverage, hedges, and time decay at high speed.

That is why the best response is usually not panic or heroics. It is context. Understand that options now play a major role in shaping daily market behavior. Respect the speed of that world without confusing it for long-term truth. And remember that a market can be noisy, twitchy, and slightly ridiculous on the surface while still rewarding patience underneath. In a strange way, that may be the most useful lesson of all: the louder the options market gets, the more valuable a calm process becomes.