Table of Contents >> Show >> Hide

- What “the bottom” actually means in real estate (and why it’s confusing on purpose)

- Why the market felt frozen: the three-headed affordability monster

- Signals we’re thawing out: the market is shifting from “stuck” to “steady”

- The likely 2026 storyline: a soft landing, not a victory parade

- What could still spoil the party (because real estate loves plot twists)

- Where “brighter days” show up first

- Practical playbook for buyers in a post-bottom market

- Practical playbook for sellers: win the new market, not the old one

- Investors and landlords: 2026 is a fundamentals year

- So… are we past the bottom?

- Experiences That Match the Moment: What “Past the Bottom” Feels Like in Real Life (Extra )

If the real estate market were a movie, the last few years would be the part where the main character stares into the mirror,

whispers “I can change,” and then immediately gets hit by an unexpected bill. Between higher mortgage rates, stubbornly high

home prices, and the “I’m not moving out of my 3% mortgage, thanks” phenomenon, the housing market has felt less like a

smooth ride and more like a shopping cart with one squeaky wheel.

But here’s the good news: markets don’t need fireworks to get better. Sometimes “better” looks like steadier, less chaotic,

more predictablelike finally finding a lane on the highway that doesn’t slam on the brakes every 12 seconds. As we move

through 2026, more data points and forecasts suggest the U.S. housing market may be past its worst stretch in activity, with

brighter (if not blinding) days ahead.

What “the bottom” actually means in real estate (and why it’s confusing on purpose)

When people say “the market hit bottom,” they often mean one of three different thingssometimes all in the same sentence:

sales volume (how many homes sell), prices (what homes cost), and sentiment

(whether buyers and sellers feel brave enough to do anything besides refresh listings at midnight).

- Sales volume bottom: This is the “nobody’s moving” phasetransactions slow, even if prices don’t crash.

- Price bottom: This is when prices stop falling (or stop rising) and stabilizeoften unevenly by region.

- Confidence bottom: The point where people stop waiting for “the perfect time” and start acting again.

In this cycle, the “bottom” has looked more like a freeze than a free-fall. Many markets didn’t see a dramatic national

price collapse; instead, they saw a sharp slowdown in sales activity and a long tug-of-war between affordability and limited supply.

Why the market felt frozen: the three-headed affordability monster

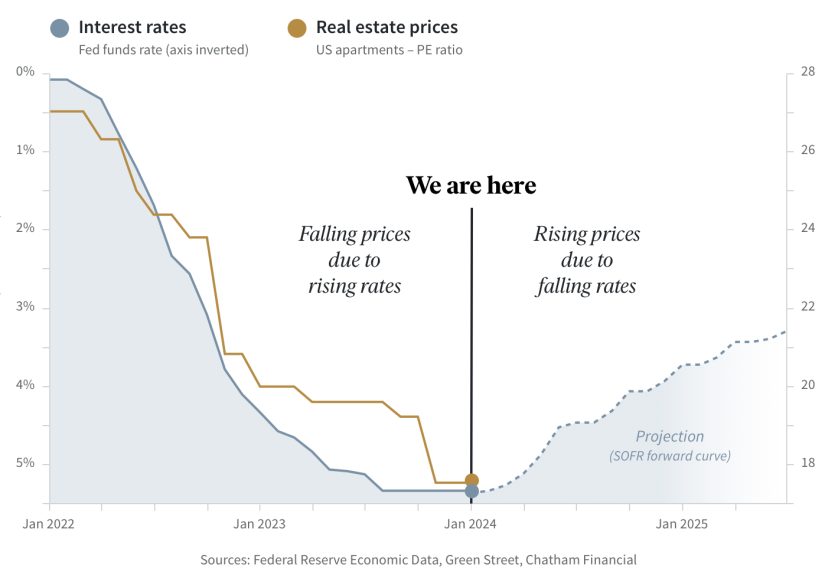

1) Mortgage rates reset the math overnight

Housing is a monthly-payment business. When mortgage rates jump, affordability can fall fasteven if home prices don’t move much.

That’s how you get the weird modern reality where a “price reduction” can still feel unaffordable, like a $10 discount on a $200

concert ticket… after fees.

2) The lock-in effect kept homeowners on the couch

Millions of homeowners are sitting on low-rate mortgages from earlier years. Trading a 3% mortgage for something north of 6% can

feel like downgrading from “premium streaming” to “free trial with 47 ads.” So many people simply stayed put, which reduced resale inventory.

And when resale inventory is tight, buyers have fewer choices and prices stay firmer than expected.

3) Inventory improved in placesbut not evenly

Some metro areas have seen noticeably more listings and more price reductions, while other markets are still tight. The result:

national headlines can be technically true while still being useless for your specific ZIP code. (Real estate is humble like that.)

Signals we’re thawing out: the market is shifting from “stuck” to “steady”

Mortgage rates have eased from their peaks

Lower rates don’t instantly fix affordability, but they can change buyer psychology and monthly payments enough to restart activity.

Even small dips matter when the loan amount is large. Rate relief also tends to unlock refinancing activity and bring some homeowners

off the sidelines.

Inventory is recovering gradually

Forecasters expect for-sale inventory to keep improving, which can reduce bidding wars and shift negotiating power. That doesn’t mean

a flood of homes, but it does mean buyers may see more options, more days on market, and more seller concessionsespecially in markets

where supply has climbed.

Prices are behaving more like “normal” again

Instead of sharp spikes, many outlooks point to modest price growth nationally in 2026. That’s important because a market

doesn’t need falling prices to feel betterwhat it needs is a world where incomes can catch up and payments don’t climb faster than paychecks.

The likely 2026 storyline: a soft landing, not a victory parade

If you’re hoping for a “back to 2021” housing market, I have bad news: that market is currently living on a farm upstate with your

childhood goldfish. The more realistic base case for 2026 is a steadier environment with incremental improvements:

slightly lower rates, slightly higher sales, modest price growth, and slow-but-real affordability gains.

Home prices: modest growth (with lots of local variation)

Several major forecasts expect home prices to rise only a little in 2026think “gentle incline,” not “rocket launch.”

That’s consistent with a market where supply improves but demand doesn’t disappear. In practical terms, it can mean fewer bidding wars,

more inspection contingencies returning, and less pressure to make decisions in 14 minutes with a shaky hand and a cold coffee.

Existing-home sales: low base, small rebound

When sales volumes have been near multi-decade lows, it doesn’t take much improvement to show growth. A small increase in affordability

and inventory can bring more deals back to life. The key is that a “better” market isn’t just about pricesit’s about mobility:

people being able to move for jobs, family needs, downsizing, upsizing, and life in general.

Affordability: improvements can happen even if prices don’t fall

Affordability can improve through a combination of wage growth, stable prices, and slightly lower rates. If payments ease while incomes

rise, the market can feel more accessible. And when the market feels more accessible, people stop waiting for a mythical “perfect bottom”

and start making decisions based on real life.

What could still spoil the party (because real estate loves plot twists)

- Rates staying higher for longer: If mortgage rates don’t drift down, affordability remains the main constraint.

- Job-market shocks: Housing is sensitive to layoffs and uncertainty. Confidence drives transactions.

-

Insurance and property-tax pressure: In some regions, rising carrying costs (taxes, insurance, HOA fees) are a bigger

deal than the mortgage rate itself. - New construction constraints: Builders can add supply, but financing costs, labor issues, and local regulations still matter.

- Regional divergence: One market can be booming while another cools. National averages hide the drama.

Where “brighter days” show up first

Real estate recoveries don’t arrive everywhere at once. They tend to show up first in places where:

(1) inventory is improving, (2) job growth is steady, and (3) homes are still comparatively attainable relative to incomes.

Markets with rising inventory and more negotiating room

In some major metros, higher inventory has shifted leverage toward buyers: longer time on market, more price cuts, and more willingness

from sellers to cover closing costs or offer rate buydowns. That’s not a “crash”that’s a market returning to basic physics:

when supply rises, buyers get choices.

“Next-to” markets and value-driven metros

Buyers often hunt for value near expensive hubsmetro areas that offer a similar lifestyle or job access without the same price tag.

These areas can outperform when people prioritize affordability and flexibility, especially as remote and hybrid work patterns continue.

Practical playbook for buyers in a post-bottom market

If you’re buying in 2026, your advantage is that you may not be competing with a stadium full of desperate bidders. Your challenge is

that affordability is still tight, so strategy matters.

Shop the rate like it’s your second job

Different lenders can quote meaningfully different rates and fees. Compare offers, ask about points, and look at the full loan estimate

not just the headline rate. (A low rate with high fees is like “free shipping” with a $39 handling charge.)

Use concessions creatively

In markets where sellers have less leverage, concessions can be a powerful tool: closing cost credits, temporary buydowns, or repairs.

The best deal isn’t always the lowest priceit’s the best overall monthly-payment and cash-to-close combo for your situation.

Be picky, but don’t be paralyzed

“Waiting for the perfect moment” is a classic trap. A smarter approach is to set clear affordability boundaries and buy when the home

fits your needs and your budgetwith a cushion. (If your budget only works when nothing ever goes wrong, it’s not a budget. It’s a wish.)

Practical playbook for sellers: win the new market, not the old one

Many sellers still remember the “list it on Thursday, accept 17 offers by Saturday” era. Today’s buyers are more payment-sensitive

and more selective. Sellers who adjust can still do well.

Price for today, not for peak season nostalgia

Overpricing is riskier in a normalizing market because buyers have more choices. A well-priced home can still attract competition,

while an overpriced one can sit, get stale, and end up chasing the market downward.

Make the home easy to say yes to

Clean, decluttered, well-lit, and repaired beats “quirky fixer-upper charm” for most buyers. Small improvementsfresh paint, lighting,

basic maintenanceoften matter more than expensive upgrades.

Plan your next move with math, not vibes

If you’re selling and buying again, focus on the net outcome: purchase price, rate, taxes, insurance, and lifestyle needs.

A “great sale” doesn’t feel great if your next monthly payment makes you flinch every time you open your banking app.

Investors and landlords: 2026 is a fundamentals year

In a modest-growth environment, investing leans more on cash flow, property quality, and risk management than quick appreciation.

This is where boring can be beautiful: conservative assumptions, realistic rent growth, and careful attention to expenses.

- Underwrite conservatively: Assume slower rent growth and higher maintenance/insurance costs.

- Prioritize durability: Locations with steady employment and diversified economies tend to be more resilient.

- Respect the “hidden” costs: Insurance, taxes, HOA rules, and local regulations can change the equation fast.

So… are we past the bottom?

If “bottom” means the worst of the market paralysisultra-low mobility, affordability shock, and buyers/sellers staring at each other

like it’s a middle-school dancethen signs point to improvement. Rates are easing compared with their highs, forecasts lean toward a

steadier 2026, and inventory recovery is giving buyers more options. That’s not a boom, but it is progress.

The brighter days ahead may look less like confetti and more like calm: a housing market where negotiations return, listings last longer

than a weekend, and decisions are made with spreadsheets instead of panic. Honestly? That sounds pretty bright.

Experiences That Match the Moment: What “Past the Bottom” Feels Like in Real Life (Extra )

“Past the bottom” is a headline. What people actually experience is a string of small momentssome hopeful, some annoying, many involving

calculators. Here’s what the shift looks like on the ground, through the kinds of stories real buyers, sellers, and homeowners keep living.

The first-time buyer who finally gets to negotiate

A couple tours their fifth open house of the month and realizes something strange: the agent isn’t saying “we already have three offers”

before they even step inside. The home has been on the market for 21 days. That number used to feel like a geological era. Now it’s just…

normal. They ask about closing cost help. The seller doesn’t laugh. They ask for an inspection contingency. The seller doesn’t faint.

When their offer is accepted, it feels less like winning the lottery and more like completing a very intense paperwork marathon.

That’s progress.

The homeowner with a low-rate mortgage who chooses remodeling over moving

A family wants another bedroom but refuses to trade their old mortgage rate for a much higher one. So they do what many homeowners do

in this environment: they renovate. Suddenly, the “starter home” becomes the “we’re-staying-here-for-a-while home.” They convert a garage,

finish a basement, or add a small extension. It’s not cheap, but compared to movingclosing costs, higher rates, and the stress of finding

a new placeit can feel like the more controllable path. The market “bottom” here doesn’t mean distress; it means people adapting.

The move-up buyer who’s patient instead of desperate

A buyer looking for a bigger home doesn’t have to sprint. They watch listings longer, see more price reductions, and learn which homes

are overpriced “test balloons.” They also see more builder incentives in some areascredits, rate buydowns, or upgradesbecause builders

want to keep demand moving. The buyer still feels the bite of higher rates, but the psychological pressure is lighter. And sometimes,

that reduced pressure is exactly what allows a smart decision instead of a rushed one.

The seller who realizes presentation is back

A seller lists their home andplot twistbuyers don’t instantly ignore the dated carpet and the “we used this room for storage since 2017”

vibes. In a post-bottom market, buyers are choosier. The seller decides to paint, declutter, and fix the small stuff. They offer a credit

for a rate buydown. Showings improve. The home sells. The lesson: today’s market rewards sellers who meet buyers where they are, not where

they were three years ago.

The renter watching rents cool while saving for a down payment

A renter notices rent increases aren’t as aggressive as they were. That doesn’t automatically make buying easy, but it can create breathing

room: more savings, less panic, more time to build credit and compare neighborhoods. For renters, “past the bottom” can feel like a return

of optionsbuy now, buy later, or keep renting without feeling like the ground is moving under their feet every lease renewal.

Put all these experiences together and you get the real meaning of “brighter days ahead”: not a perfect market, but a more workable one.

A market where people can plan again. And in real estate, being able to plan is practically a superpower.