Table of Contents >> Show >> Hide

- Why Interest Rates and Inflation Matter for Stock Valuations

- How Interest Rates Move the Valuation Dial

- Inflation’s Complicated Relationship With Stock Valuations

- Rates, Inflation, and Today’s Market: Why Valuations Still Look Rich

- A Wealth of Common Sense Approach to Valuations

- Real-World Experiences and Lessons Learned

- Bringing It All Together

If you’ve ever stared at the stock market and thought, “Why on earth are prices doing that today?”,

there’s a good chance interest rates and inflation are somewhere behind the scenes, pulling invisible strings.

You don’t need a PhD in economics to understand what’s going onyou mostly need a bit of math, a bit of history,

and a healthy dose of common sense.

In this guide, we’ll unpack how interest rates and inflation really affect stock market valuations,

why sometimes high rates don’t tank stocks (and low rates don’t guarantee a party), and how to think

about valuations without losing your mindor your long-term plan. Think of this as

a “Wealth of Common Sense” tour through the chaos.

Why Interest Rates and Inflation Matter for Stock Valuations

Stock prices are basically a big bet on a company’s future cash flows. When you buy a stock, you’re paying today

for profits that (hopefully) arrive over many years. Valuation is about

turning that messy future into a single number you’re willing to pay now.

Valuation 101: From Cash Flows to Price Tags

At the heart of most valuation models is a simple idea:

- Estimate future cash flows (earnings, dividends, free cash flow).

- Decide what return you require to own the stock (your “discount rate”).

- Discount those future cash flows back to today.

The higher the discount rate, the less those future dollars are worth today.

That’s why interest rates matter so much. They’re a major building block of that required return.

On top of that, inflation changes both sides of the equation: it can affect the cash flows themselves

(through costs, prices, and profit margins) and the return investors demand to keep up with rising prices.

In the real world, most investors don’t run discounted cash flow spreadsheets every morning.

Instead, they look at valuation multiples like:

- Price-to-earnings (P/E): How many dollars you pay for each dollar of earnings.

- Price-to-sales (P/S): How many dollars you pay for each dollar of revenue.

- EV/EBITDA or price-to-book: Other shortcuts to compare companies and markets.

Whether you’re using a spreadsheet or a shorthand multiple, the logic is the same: when interest rates

and inflation change, the trade-off between risk, return, and future growth shiftsand valuations shift with it.

How Interest Rates Move the Valuation Dial

Interest ratesespecially long-term government bond yieldsare often treated as the “gravity” of financial markets.

When gravity is low (rates are low), asset prices can float higher. When gravity increases, valuations get pulled back to earth.

The Discount Rate Effect: Higher Rates, Lower Present Values

Most valuation models use something like this idea:

Present value = Future cash flow ÷ (1 + discount rate)years

If the discount rate goes upbecause bond yields rise, credit spreads widen, or investors become more risk averse

the denominator gets bigger and today’s value of those future earnings falls. That’s the mechanical reason

why rising interest rates tend to pressure stock valuations.

Growth stocks, whose profits are expected far in the future, are particularly sensitive. They’re “long-duration” assets:

most of their value depends on earnings many years from now. When the discount rate rises, those far-off cash flows get hit hardest,

and valuations can compress quickly. Value stocks, with more cash flow upfront and often higher current yields, are usually less sensitive.

The Competition Effect: When Bonds Stop Being Boring

There’s another common-sense effect: competition for your money.

In a world of near-zero interest rates, cash and bonds feel like they pay nothing.

That’s when the old line “There Is No Alternative” (TINA) to stocks shows up in market commentary.

Investors may be willing to accept lower earnings yields (higher P/E ratios) because the alternativeTreasuries or savings accountslooks terrible.

When short-term yields and bond coupons rise, suddenly there is an alternative.

Call it the TARA world: “There Are Reasonable Alternatives.” If you can earn 4–5% (or more) in a relatively safe bond,

you might not be thrilled to accept a 4% earnings yield (a 25x P/E) on a stock index with real business risk and volatility.

This trade-off is captured in the idea of the equity risk premiumthe extra return investors demand over

risk-free rates to hold stocks. When interest rates rise, investors may insist on a higher equity risk premium.

That usually means paying lower multiples for the same earnings, even if profits haven’t changed.

Which Sectors Feel Interest Rate Changes the Most?

Not all parts of the market react the same way when rates move:

-

Growth and “long-duration” stocks (think high-valuation tech) tend to be hit hardest when rates rise.

Their profits are further out in the future, so the discounting effect is stronger. -

Value stocks and companies with strong current cash flows can sometimes hold up better.

They feel less pain from higher discount rates, and some can pass on higher borrowing costs through pricing power. - Financials may benefit from higher interest margins when rates rise, though credit quality and loan demand also matter.

-

Real estate and utilities often behave like bond proxieshigher rates can hurt, because their dividends

are compared directly to bond yields.

The big picture: interest rates don’t move all stocks equally; they reshuffle the deck.

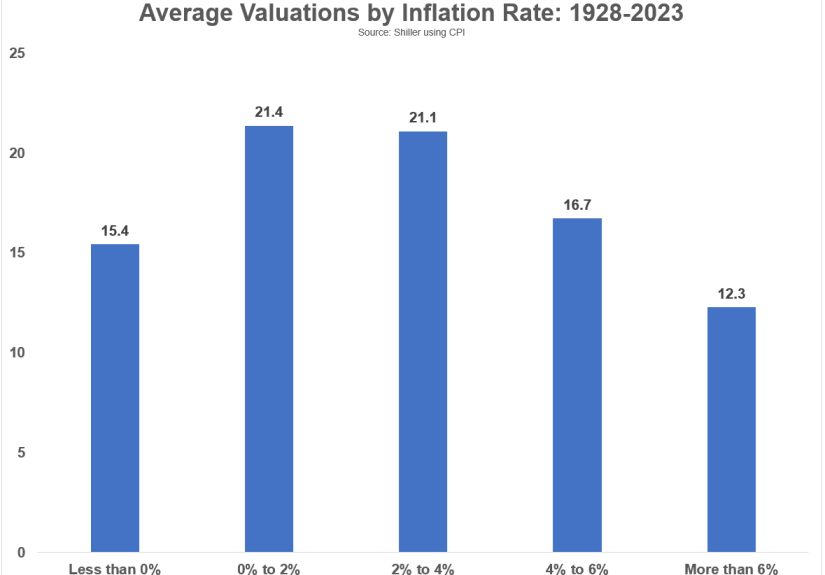

Inflation’s Complicated Relationship With Stock Valuations

Inflation is like salt in a recipe: a little bit can make the dish better, but too much ruins itand

too little can be a problem in its own way. The stock market feels similarly about price levels.

Moderate, Stable Inflation: The Goldilocks Zone

Historically, stock markets have done well in periods of low to moderate, stable inflation.

In that environment:

- Companies can raise prices gradually to offset rising costs.

- Earnings and dividends often grow in nominal terms.

- Uncertainty about future purchasing power is manageable, which helps support higher valuation multiples.

When inflation is predictable, analysts can model future margins and cash flows with more confidence.

That comfort shows up as higher P/E ratios and tighter risk premiums.

The market may even reward companies for steady inflation-linked growth.

High or Unstable Inflation: The Valuation Killer

High inflation, especially when it’s volatile or rising, tends to be poison for valuation multiples.

There are several reasons:

- Uncertainty jumps: It’s harder to forecast costs, pricing power, and real earnings.

- Real earnings growth may slow: Input costs can outrun a company’s ability to raise prices.

- Required returns rise: Investors demand a higher nominal return to keep up with inflation,

which pushes up discount rates and pushes down valuations.

Empirical research has long found a negative relationship between high expected inflation and stock valuations,

especially P/E ratios. When inflation spikes, the market often demands a cheaper entry point to compensate for the messier outlook.

And just to make things more fun, inflation often invites central banks into the picture.

If a central bank responds with aggressive rate hikes, you get a double whammy: higher inflation and higher nominal rates,

both of which tend to weigh on valuationsat least in the short run.

Very Low Inflation or Deflation: Not Always Good News

At the other extreme, very low inflation or deflation isn’t always bullish either.

Falling prices can be a symptom of weak demand, stagnant earnings, or economic stress.

In those environments, nominal interest rates can hit the zero lower bound, and growth expectations may be subdued.

That’s why markets often prefer “boringly positive” inflationenough to support growth and wage gains,

but not so much that people start hoarding canned goods and complaining about shrinkflation in every aisle.

Rates, Inflation, and Today’s Market: Why Valuations Still Look Rich

In recent years, investors have had to navigate a bizarre combination of:

- Rapidly rising interest rates from near-zero levels.

- Inflation that spiked, then started to coolbut stayed above central bank targets for a while.

- Stock markets that, despite all the worry, continued to trade at elevated valuation multiples in many segments.

How does that square with the theory that higher rates and elevated inflation should pull valuations down?

A few forces help explain the resilience:

- Strong earnings growth in key sectors, especially technology and AI-related companies.

- High profit margins fueled by years of cheap capital, productivity gains, and pricing power.

- Persistent optimism about long-term innovation and productivity from new technologies.

In other words, markets are not just a spreadsheet of rates and inflationthey also reflect narratives,

investor psychology, and expectations about future growth. That’s a theme repeated often by thoughtful commentators:

rates and inflation matter a lot, but they don’t operate in a vacuum. Earnings, risk appetite, and structural trends

(like demographics and technology) all mix into the valuation stew.

A Wealth of Common Sense Approach to Valuations

So how do you use all this without turning investing into a full-time macro guessing game?

Here’s a common-sense framework:

1. Recognize That Valuations Are a Function of the Environment

When rates are near zero and inflation is tame, higher valuation multiples aren’t shockingthey’re a logical response

to cheaper capital and a scarcity of yield elsewhere. When rates rise and inflation is noisy, you should expect

some valuation compression or at least less multiple expansion.

The mistake is assuming that valuations “must” revert on your schedule.

Markets can stay richly valued for years if earnings keep rising or if investors keep believing that the future will be better than the recent past.

2. Think in Terms of Ranges, Not Single “Fair Value” Numbers

A lot of valuation debates get stuck on specific numbers: “The market should trade at 15x earnings, not 21x.”

In reality, reasonable fair-value ranges shift with rates, inflation, and earnings trends.

A 21x multiple might be excessive in one environment and completely rational in another.

Instead of asking, “What’s the one correct P/E?” it’s more useful to ask:

- Given current rates, what’s a reasonable earnings yield?

- How much equity risk premium am I really getting?

- Are current margins and growth assumptions realistic, or are we assuming perfection?

3. Focus on Earnings Power and Balance Sheets

Over long periods, stock returns are driven by earnings growth and the level of valuations you start from.

You can’t control the macro, but you can pay attention to:

- Whether a company can maintain or grow real earnings in different inflation environments.

- How sensitive it is to higher borrowing costs (debt-heavy vs. cash-rich).

- Whether its business model has pricing power or is stuck in a race to the bottom.

In a world where rates and inflation swing around, durable earnings power and strong balance sheets

become a kind of shock absorber for valuations.

4. Don’t Use Macro as an Excuse to Never Invest

One of the most damaging habits investors fall into is waiting for perfect macro conditions before investing.

“I’ll buy when inflation settles down.” “I’ll buy when the Fed stops hiking.” “I’ll buy when valuations get cheap again.”

The problem: markets often start moving long before the data looks comfortable.

By the time inflation feels under control and headlines are calm, much of the recovery may already be priced in.

Using rates and inflation as a compass is smart. Using them as a reason to stay on the sidelines indefinitely is not.

Real-World Experiences and Lessons Learned

Theory is helpful, but lived experience is where the lessons really stick.

Here are a few composite stories that capture how interest rates, inflation, and valuations feel from the front row.

Case Study 1: The Growth Investor in a Rising-Rate World

Alex built a portfolio in the era of ultra-low interest rates. Their holdings were packed with high-growth tech,

software-as-a-service names, and companies forecast to be massively profitablesomeday. Valuations didn’t look cheap,

but when 10-year Treasury yields hovered near 1%, a 40x or 50x earnings multiple felt almost normal.

Then rates started rising quickly. Suddenly, the discounted cash flow models that once justified sky-high valuations

looked different. A modest bump in the discount rate translated into a sharp drop in present value,

especially for those companies with most of their earnings projected a decade out.

Many of Alex’s positions fell 30–60%, even though the businesses were still growing.

The painful takeaway for Alex wasn’t “growth is bad.” It was more nuanced:

- When you pay a lot for future growth, your margin of safety depends heavily on interest rates staying friendly.

- Even great businesses can be lousy investments if the starting valuation assumes perfection.

- Rate regimes change, and portfolios should be built with that possibility in mind.

Case Study 2: The Dividend Investor Who Forgot About Inflation

Maria liked simplicity. She focused on dividends and loved seeing cash land in her account each quarter.

For years, she held a mix of high-yield stocks and utility names. When inflation was low, collecting a 3–4% yield

felt like a comfortable strategy.

Then inflation surged. Prices at the grocery store and gas pump soared, and suddenly that 3–4% yield didn’t feel

so generous anymore. At the same time, newly issued bonds and CDs started offering higher yields,

and some of Maria’s dividend payers lagged on increasing payouts. Her real (after-inflation) income was shrinking.

What Maria learned:

- Nominal yields can be deceptive; real yields (after inflation) matter more to purchasing power.

- Companies with a history of growing dividends in real terms are better inflation companions than static high yielders.

- Inflation risk is just as important as interest rate risk in retirement planning.

Case Study 3: The Long-Term Investor Who Stayed Systematic

Jordan didn’t try to forecast every macro twist. Instead, they followed a disciplined plan:

- Regular contributions into a diversified portfolio of stocks and bonds.

- Periodic rebalancing, trimming what had run up and adding to what had lagged.

- A focus on long-term after-inflation returns rather than short-term market noise.

Over a decade, Jordan lived through:

- Falling rates and rising valuations.

- A surge in inflation and sharp rate hikes.

- Scary headlines predicting both runaway inflation and imminent deflation at different points.

Did Jordan’s portfolio bounce around? Absolutely. Did valuations expand and contract? Constantly.

But by staying invested, rebalancing systematically, and resisting the urge to time every macro move,

Jordan captured the market’s long-term growth while avoiding the biggest behavioral mistakes.

Their conclusion was refreshingly simple:

understand how interest rates and inflation influence valuations,

but don’t let them control your entire strategy. Use them as context, not as a crystal ball.

Bringing It All Together

Interest rates and inflation are powerful forces in the market. They shape discount rates, feed into the equity risk premium,

influence which sectors thrive, and help determine how much investors are willing to pay for a dollar of earnings.

But they are not destiny. Earnings growth, innovation, corporate balance sheets, and plain old human psychology

can overpower simple models for long stretches of time. That’s why a “wealth of common sense” approach to investing

doesn’t obsess over every rate move or CPI release. Instead, it:

- Respects how valuations respond to changing macro conditions.

- Avoids overpaying for perfection in any environment.

- Focuses on long-term, inflation-aware returns and durable businesses.

- Stays diversified and disciplined, even when headlines scream otherwise.

In short: watch interest rates and inflation closely, but let common sensenot feardrive your investment decisions.